Donald R. van Deventer[1] First Version: October 6, 2021 This Version: October 6, 2021 ABSTRACT Please note: Kamakura...

Donald R. van Deventer[1] First Version: October 6, 2021 This Version: October 6, 2021 ABSTRACT Please note: Kamakura...

In a recent post on SeekingAlpha, we pointed out that a forecast of “heads” or “tails” in a coin flip leaves out critical...

Donald R. van Deventer[1] First Version: September 28, 2021 This Version: September 30, 2021 ABSTRACT Please note: Kamakura...

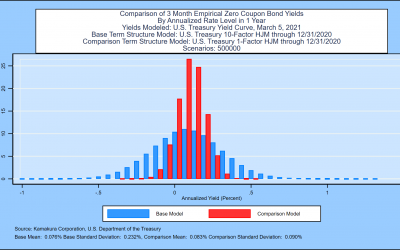

Donald R. van Deventer[1] First Version: September 21, 2021 This Version: September 22, 2021 ABSTRACT Please note: Kamakura...

In a recent post on SeekingAlpha, we pointed out that a forecast of “heads” or “tails” in a coin flip leaves out critical...

In a recent post on SeekingAlpha, we pointed out that a forecast of “heads” or “tails” in a coin flip leaves out critical...

In a recent post on SeekingAlpha, we pointed out that a forecast of “heads” or “tails” in a coin flip leaves out critical...

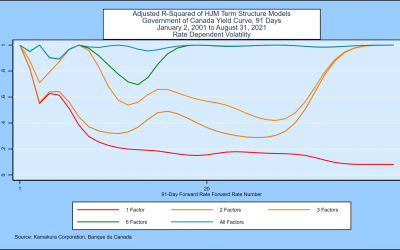

Model Validation: Proof that 1-factor Interest Rate Models Underestimate Risk by 61% to 83% Donald R. van Deventer[1] First...

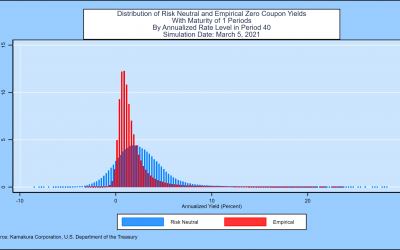

A 10 Factor Heath, Jarrow and Morton Stochastic Volatility Model for the U.S. Treasury Yield Curve, Using Daily Data from...

ABSTRACT This paper analyzes the number and the nature of factors driving the movements in the Japanese Government Bond yield...

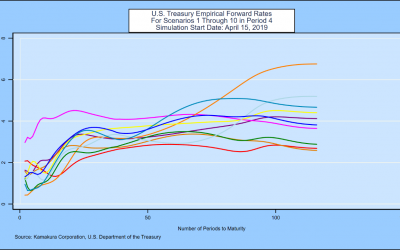

ABSTRACT This paper analyzes the number and the nature of factors driving the movements in the U.S. Treasury yield curve from...

ABSTRACT This paper analyzes the number and the nature of factors driving the movements in the German Bund yield curve from...