TROUBLED COMPANY INDEX®

The Troubled Company Index ® measures the percentage of 42,500 public firms in 76 countries that have an annualized one-month default risk of over one percent.

HJM++© Correlated Government Yield and Foreign Exchange Rate Simulations for Asia-Pacific, Europe and North America, August 7, 2026

The Heath, Jarrow and Morton [1992] framework for simulation and valuation using risk-free interest rates has been called “the most important paper in financial economics in the last 50 years.” The Center for Applied Quantitative Finance provides the risk-neutral and...

SAS Weekly Treasury Simulation, August 7, 2026: Probability of 3-Month Bill Yield Over 4% in One Year Drops 19% to 35%

Summary The most likely range for 3-month bill yields in 10 years remained at the 1% to 2% range this week. The probability of being in this range is 0.94% higher than the probability of being in the 0% to 1% range. Treasury 2-year yields moved to 4.19% this week from...

SAS Weekly Treasury Simulation, July 31, 2026: 54% Probability of 3-Month Bill Yield Over 4% in One Year

Summary The most likely range for 3-month bill yields in 10 years remained at the 1% to 2% range this week. The probability of being in this range is 0.91% higher than the probability of being in the 0% to 1% range. Treasury 2-year yields moved to 4.28% this week from...

SAS Weekly Treasury Simulation, July 24, 2026: 53% Probability of 3-Month Bill Yield Over 4% in One Year

Summary The most likely range for 3-month bill yields in 10 years remained at the 1% to 2% range this week. The probability of being in this range is 0.82% higher than the probability of being in the 0% to 1% range. Treasury 2-year yields moved to 4.33% this week from...

SAS Weekly Treasury Simulation, July 17, 2026: 42% Probability of 3-Month Bill Yield Over 4% in One Year

Summary The most likely range for 3-month bill yields in 10 years remained at the 1% to 2% range this week. The probability of being in this range is 0.70% higher than the probability of being in the 0% to 1% range. Treasury 2-year yields moved to 4.18% this week from...

Update to Regional Credit Risk Analysis

Two months ago, we examined the impact of the Iran war on corporate credit risk forecasts around the world. The analysis showed that after the initial jump in March, most markets retraced much of the move by April. Out of 9 countries examined, Japan, Qatar, and Korea...

The SaaSpocalypse Impact on Credit

For much of 2026, one question has dominated the technology sector: what happens to traditional software companies when artificial intelligence can write code, automate workflows, and allow customers to build applications themselves? The resulting concern manifested...

Communication Services: The Sector Where Scale Hides the Tail

Sector dispersion has been a recurring theme in the monthly Credit Conditions Newsletter because distributional dynamics often say more about credit risk than sector averages. Two months ago, we highlighted the widening of default-probability distributions following...

Global Credit Risk After the Iran War Shock

This month we take a global look at the impact of the Iran war on corporate credit risk via analysis of median probability of default (PD) for a select group of countries. The initial corporate credit response to the Iran war shock was broad. Median 1yr PD rose across...

Iran Shock Meets a Frozen Labor Market

The Iran-war energy shock arrived at a fragile moment in the U.S. labor market. It was not because layoffs were surging, but because the labor market had shifted into a “low-hire, low-fire” equilibrium. The driving forces behind the unusual labor situation have been a...

ANALYTICS

KRIS Default Probabilities versus Credit Ratings

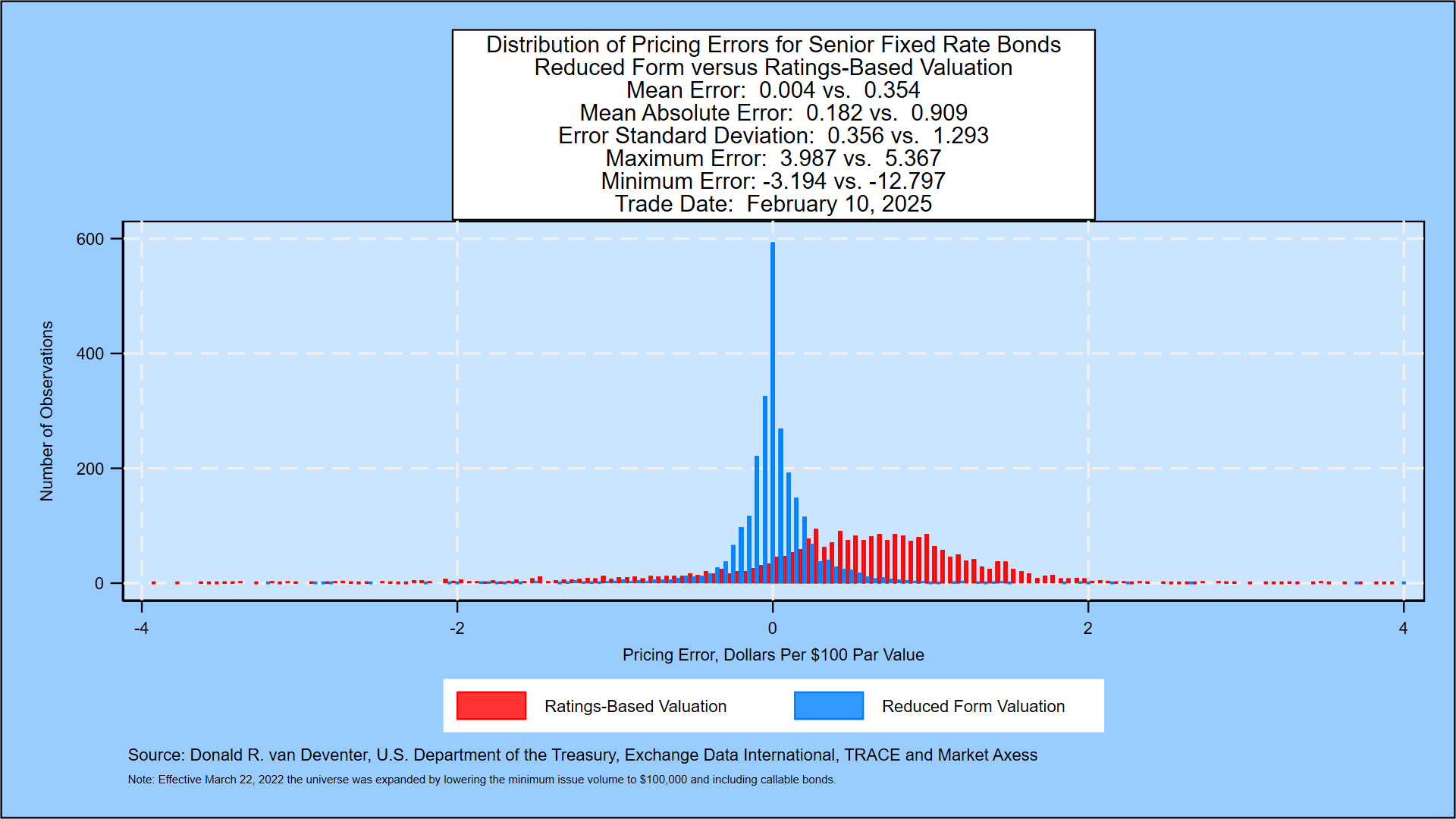

SAS Daily Bond Performance Attribution

KRIS Daily Default Probability and

Bond Cross-Validation

EVENTS

- October

- 1 OCTOBER | BattleFin Discovery Day London

- November

- 16 – 19 NOVEMBER | Quant Minds