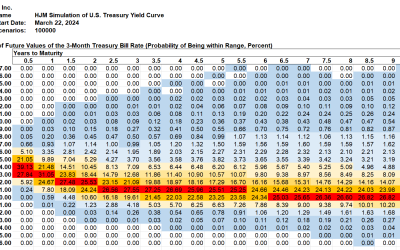

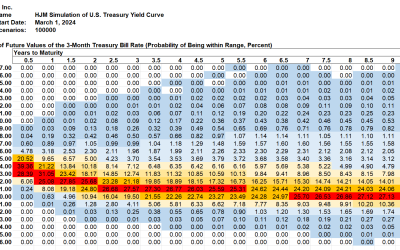

Summary The Treasury curve moved down 13 basis points at 2 years and moved down 9 basis points at 10 years over the last week....

Summary The Treasury curve moved down 13 basis points at 2 years and moved down 9 basis points at 10 years over the last week....

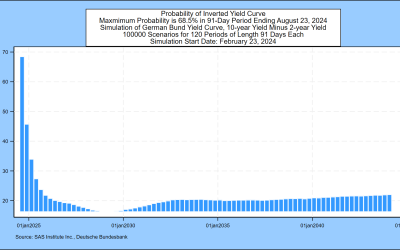

Summary The inverted Bund yields continued this week with the negative 2-year/10-year yield spread at negative 46.9 basis points...

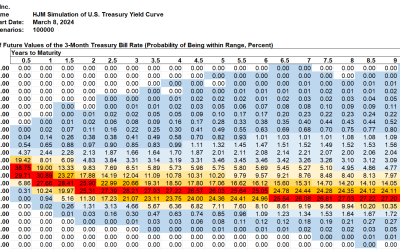

Summary The Treasury curve moved down 6 basis points at 2 years and was down 10 basis points at 10 years over the last week. As...

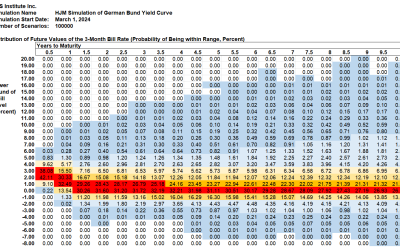

Summary The inverted Bund yields continued this week with the negative 2-year/10-year yield spread at negative 46.7 basis points...

Summary The Treasury curve moved down 13 basis points at 2 years and was down 7 basis points at 10 years over the last week. As...

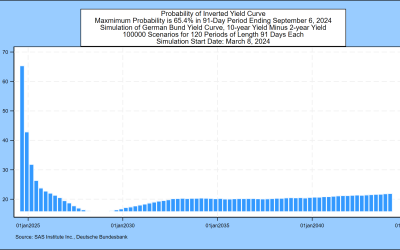

Summary The inverted Bund yields continued this week with the negative 2-year/10-year yield spread at negative 50.1 basis points...

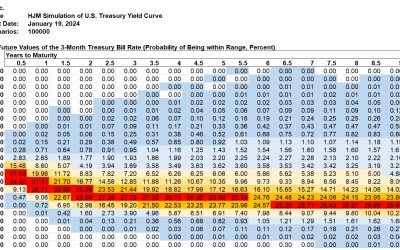

Summary The Treasury curve moved up 2 basis points at 2 years and was down 12 basis points at 10 years over the last week. As a...

Summary The Treasury curve moved up 25 basis points at 2 years and up 19 basis points at 10 years over the last week. As a...

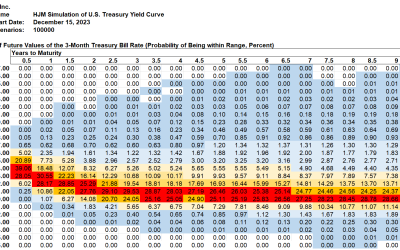

Summary The Treasury curve moved down 27 basis points at 2 years and down 32 basis points at 10 years over the last week. As a...

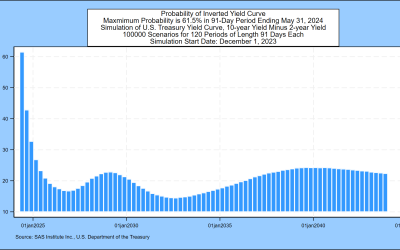

Summary The probability that the 2-year/10-year Treasury spread is still negative in the 13 weeks ending May 31, 2024 is 61.5%,...

The Valuation of Corporate Coupon Bonds Jens Hilscher, Robert A. Jarrow, and Donald R. van Deventer Updated October 12, 2023...

Robert A. Jarrow and Donald R. van Deventer A Revised Version of this Note is Forthcoming in the Journal of Fixed Income ...