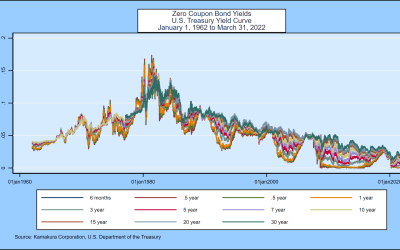

Inverted Yields, Negative Rates, and U.S. Treasury Probabilities 10 Years Forward The outlook for long-run Treasury yields...

Inverted Yields, Negative Rates, and U.S. Treasury Probabilities 10 Years Forward The outlook for long-run Treasury yields...

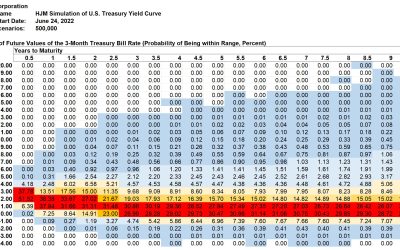

Inverted Yields, Negative Rates, and U.S. Treasury Probabilities 10 Years Forward In the aftermath of the Fed’s rate hike last...

Inverted Yields, Negative Rates, and U.S. Treasury Probabilities 10 Years Forward The Fed’s 75 basis point rate hike last week...

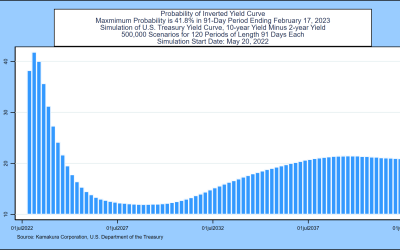

Inverted Yields, Negative Rates, and U.S. Treasury Probabilities 10 Years Forward The probability of an inverted yield curve...

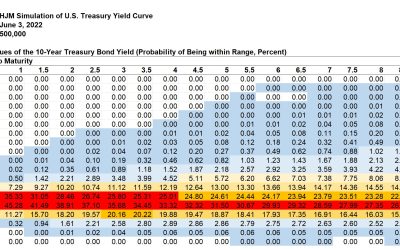

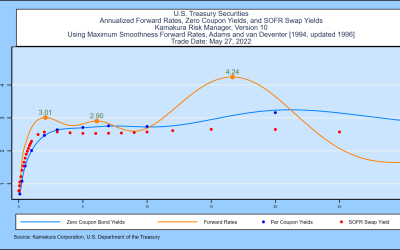

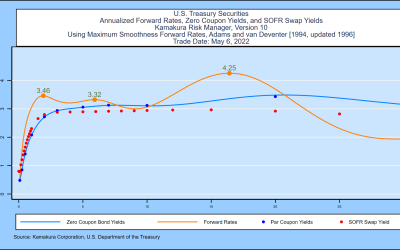

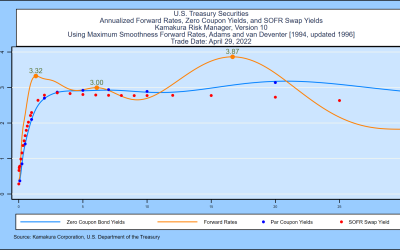

Inverted Yields, Negative Rates, and U.S. Treasury Probabilities 10 Years Forward The peak in forward rates underlying the U.S....

Inverted Yields, Negative Rates, and U.S. Treasury Probabilities 10 Years Forward The peak in forward rates underlying the U.S....

Inverted Yields, Negative Rates, and U.S. Treasury Probabilities 10 Years Forward The peak in forward rates underlying the U.S....

Robert A. Jarrow[1] and Donald R. van Deventer[2] Presentation to Risk Americas, May 11, 2022 This Version: May 19, 2022...

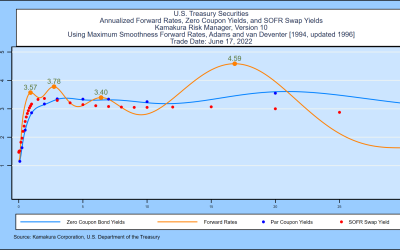

Inverted Yields, Negative Rates, and U.S. Treasury Probabilities 10 Years Forward Forward rates underlying the U.S. Treasury...

Inverted Yields, Negative Rates, and U.S. Treasury Probabilities 10 Years Forward Forward rates underlying the U.S. Treasury...

Donald R. van Deventer[1] First Version: April 15, 2022 This Version: May 2, 2022 ABSTRACT Please note: Kamakura Corporation...

Inverted Yields, Negative Rates, and U.S. Treasury Probabilities 10 Years Forward The mood in fixed income markets, waiting for...