Summary The most likely range for 3-month bill yields is again the 1% to 2% range, just 20 basis points more likely than the 0%...

Summary The most likely range for 3-month bill yields is again the 1% to 2% range, just 20 basis points more likely than the 0%...

Summary One-month forward Australian Government Bond rates peaked at 5.48% this week, compared to 5.39% the previous week. The...

Summary One-month forward New Zealand Treasury Bond rates peaked at 6.39% this week, compared to 6.27% the previous week. The...

Summary The most likely range for 3-month bill yields is again the 1% to 2% range, just 6 basis points more likely than the 0%...

Summary One-month forward New Zealand Treasury Bond rates peaked at 6.27% this week. The 2-year/10-year New Zealand Treasury...

Summary The most likely range for 3-month bill yields is again the 1% to 2% range, just 12 basis points more likely than the 0%...

Summary The most likely range for 3-month bill yields is again the 1% to 2% range, just 10 basis points more likely than the 0%...

Summary The most likely range for 3-month bill yields edged into the 1% to 2% range, just 1 basis point more likely than the 0%...

Summary The median level for the yen-U.S. dollar exchange rate is 145.18 one year from now, compared to 148.58 last week,...

Summary The most likely range for 3-month bill yields edged into the 1% to 2% range, just 1 basis point more likely than the 0%...

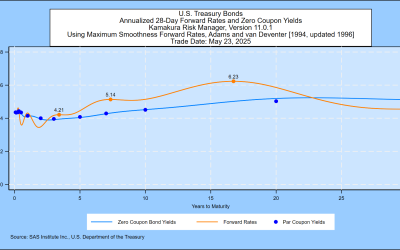

Summary Treasury 2-year yields moved to 3.68% this week from 3.89% last week. At 10 years, this week’s yield is 4.01%, compared...

Summary One-month forward New Zealand Treasury Bond rates peaked at 6.27% this week, compared to 5.87% the previous week. The...