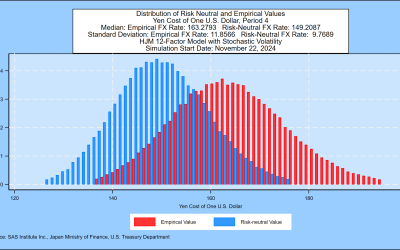

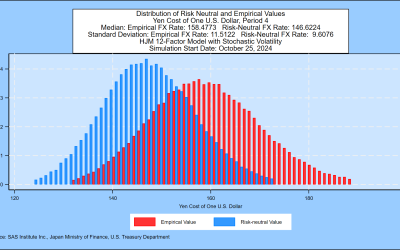

Summary The median level for the yen-U.S. dollar exchange rate is 163.28 one year from now, compared to 161.65 last week,...

Summary The median level for the yen-U.S. dollar exchange rate is 163.28 one year from now, compared to 161.65 last week,...

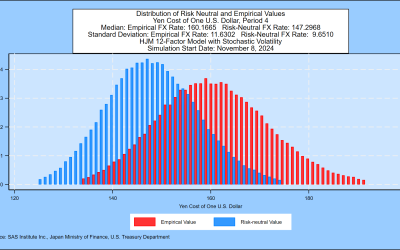

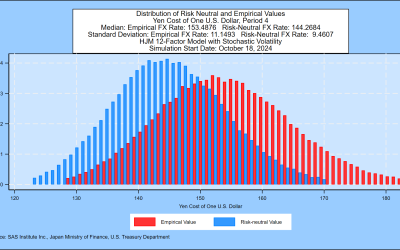

Summary The median level for the yen-U.S. dollar exchange rate is 161.65 one year from now, compared to 160 last week, according...

Summary The median level for the yen-U.S. dollar exchange rate is above 160 one year from now, compared to 158 last week,...

Summary The median level for the yen-U.S. dollar exchange rate is above 160 one year from now, up from 158 last week, according...

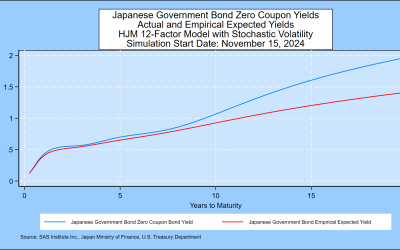

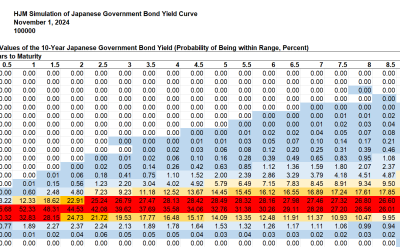

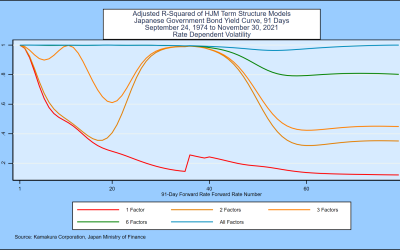

Summary The term premium in the Japanese Government Bond yield curve continues to be close to zero for the first 10 years, but...

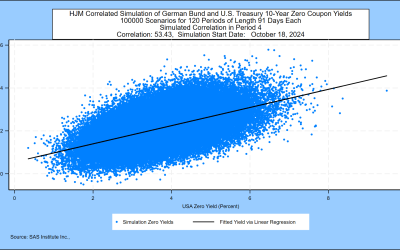

Summary During a rare quiet period, Treasury yields were unchanged at 2 years and 10 years over the last week. As a result, the...

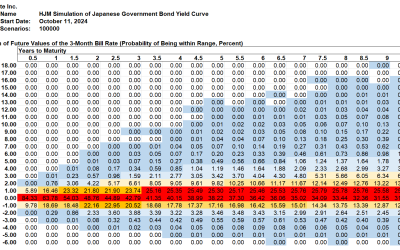

Summary The term premium in the Japanese Government Bond yield curve continues to be close to zero for the first 10 years, but...

Summary The term premium in the Japanese Government Bond yield curve is close to zero for the first 10 years, but it increases...

Summary The term premium in the Japanese Government Bond yield curve is close to zero for the first 10 years, but it increases...

Daniel Dickler, Robert A. Jarrow, Stas Melnikov, Alexandre Telnov, Donald R. van Deventer and Xiaoming Wang[1] First Version:...

Donald R. van Deventer[1] First Version: December 6, 2021 This Version: December 7, 2021 ABSTRACT Please note: Kamakura...

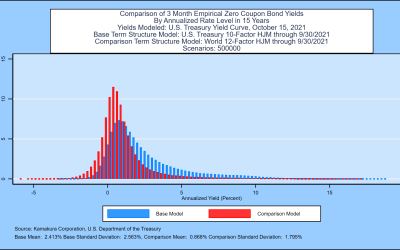

Donald R. van Deventer[1] First Version: October 19, 2021 This Version: October 21, 2021 ABSTRACT Please note: Kamakura...