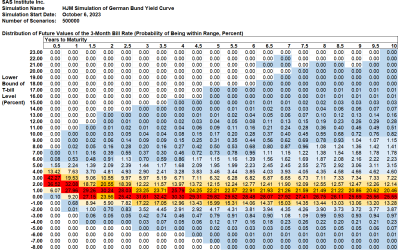

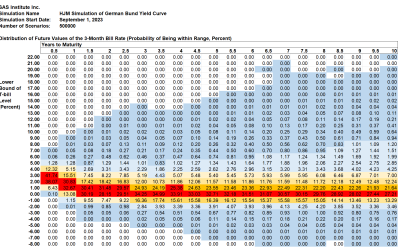

Summary The probability of a quick end to inverted Bund yields jumped up as the current negative 2-year/10-year yield spread...

Summary The probability of a quick end to inverted Bund yields jumped up as the current negative 2-year/10-year yield spread...

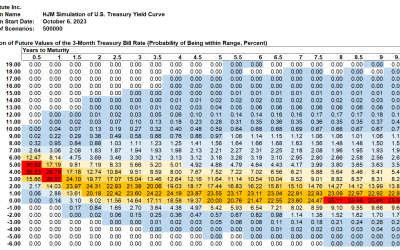

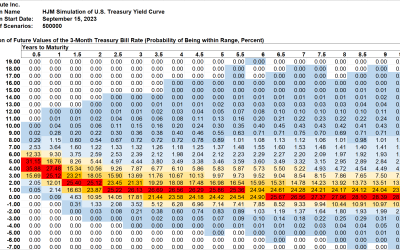

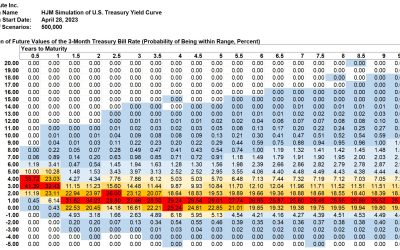

Summary The long-term peak in 1-month forward Treasuries is now 6.17%, well above the near-term peak at 5.61%. The simulated...

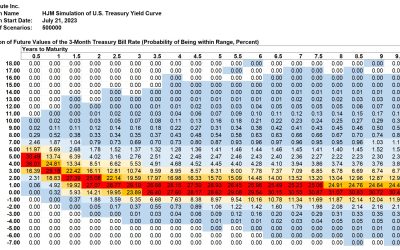

Summary The long-term peak in 1-month forward Treasuries is now 5.95%, well above the near-term peak at 5.54%. That is an...

Summary The probability of a quick end to inverted Bund yields bounced back up this week as the current negative 2-year/10-year...

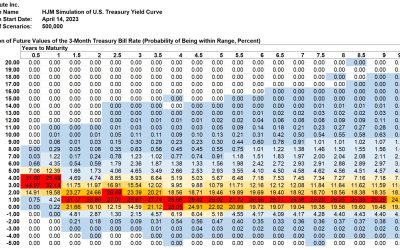

Summary The long-term peak in 1-month forward Treasuries is now 5.58%, just above the near-term peak at 5.54%. The simulated...

Summary The probability of a quick end to inverted Bund yields dropped substantially this week as the current negative...

Summary The level of 1-month forward rates implied by the current Treasury yield curve ranges from 4% to 6% for 20 years. The...

Summary 28-day Bund forward rate peaks in the short-term (3.67%) and long-term (3.59%) moved closer together this week. This...

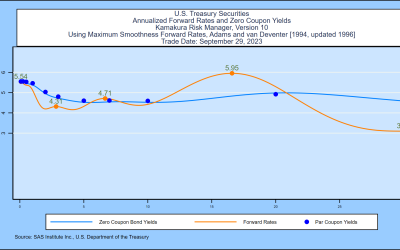

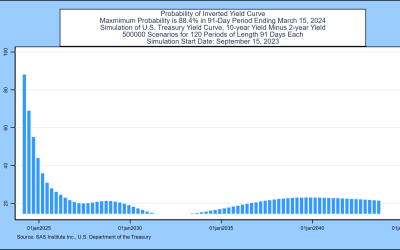

This week’s twist in the U.S. Treasury 1-month forward rate curve reveals an important stepping stone toward normal yields. The...

The streak of negative 2-year/10-year Treasury spreads has now reached 262 trading days, 16 trading days from the second longest...

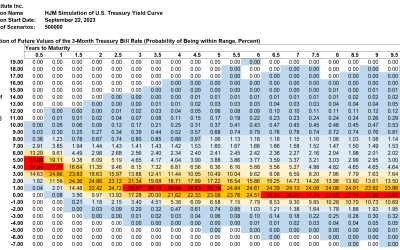

Both implied forward Treasury 1-month bill rates and simulated 3-month bill rates show high volatility and a sharp downshift,...

Both implied forward Treasury 1-month bill rates and simulated 3-month bill rates show high volatility and a sharp downshift,...