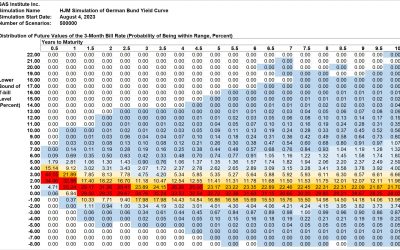

Summary The Bund 2-year/10-year spread widened to a negative 47.8 basis points from negative 42.2 basis points last week As a...

Summary The Bund 2-year/10-year spread widened to a negative 47.8 basis points from negative 42.2 basis points last week As a...

Author’s Note This simulation has been done jointly with a U.S. Treasury yield simulation in a way that reflects the correlation...

Author’s Note This simulation has been done jointly with a U.S. Treasury yield simulation in a way that reflects the correlation...

Author’s Note This simulation has been done jointly with a U.S. Treasury yield simulation in a way that reflects the correlation...

Author’s Note This simulation has been done jointly with a U.S. Treasury yield simulation in a way that reflects the correlation...

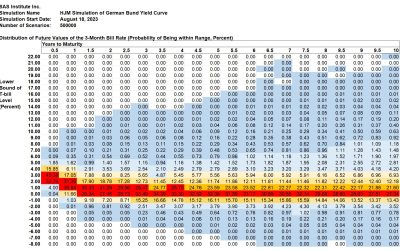

This week’s 2-year/10-year Bund yield spread is a negative 66.5 basis points, compared to a negative 86.2 basis points last...

This week’s simulation shows that the current negative 2-year/10-year Bund yield spread currently a negative 86.2 bsis points,...

This week’s simulation shows that the current negative 2-year/10-year Bund yield spread is very likely to persist at least...

Daniel Dickler, Robert A. Jarrow, Stas Melnikov, Alexandre Telnov, Donald R. van Deventer, and Xiaoming Wang[1] First Version:...

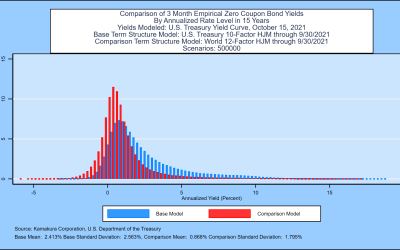

Donald R. van Deventer[1] First Version: October 19, 2021 This Version: October 21, 2021 ABSTRACT Please note: Kamakura...

Donald R. van Deventer[1] First Version: October 6, 2021 This Version: October 6, 2021 ABSTRACT Please note: Kamakura...