Daniel Dickler, Robert Jarrow, Stas Melnikov, Alexandre Telnov, Donald R. van Deventer and Xiaoming Wang[1] First Version: April...

Daniel Dickler, Robert Jarrow, Stas Melnikov, Alexandre Telnov, Donald R. van Deventer and Xiaoming Wang[1] First Version: April...

Daniel Dickler, Robert A. Jarrow, Stas Melnikov, Alexandre Telnov, Donald R. van Deventer and Xiaoming Wang[1] First Version:...

Donald R. van Deventer[1] First Version: March 8, 2022 This Version: March 8, 2022 ABSTRACT Please note: Kamakura Corporation...

Donald R. van Deventer[1] First Version: March 8, 2022 This Version: March 8, 2022 ABSTRACT Please note: Kamakura Corporation...

Donald R. van Deventer First Version: January 24, 2022 This Version: January 25, 2022 ABSTRACT Please note: Kamakura...

Donald R. van Deventer[1] First Version: December 6, 2021 This Version: December 7, 2021 ABSTRACT Please note: Kamakura...

Donald R. van Deventer[1] First Version: October 19, 2021 This Version: October 21, 2021 ABSTRACT Please note: Kamakura...

Donald R. van Deventer[1] First Version: October 12, 2021 This Version: October 13, 2021 ABSTRACT Please note: Kamakura...

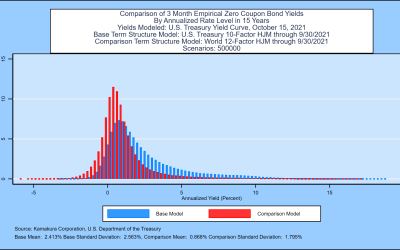

Donald R. van Deventer[1] First Version: October 6, 2021 This Version: October 6, 2021 ABSTRACT Please note: Kamakura...

Donald R. van Deventer[1] First Version: September 28, 2021 This Version: September 30, 2021 ABSTRACT Please note: Kamakura...

Donald R. van Deventer[1] First Version: September 21, 2021 This Version: September 22, 2021 ABSTRACT Please note: Kamakura...

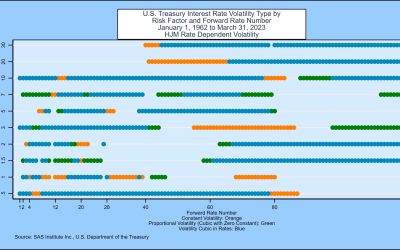

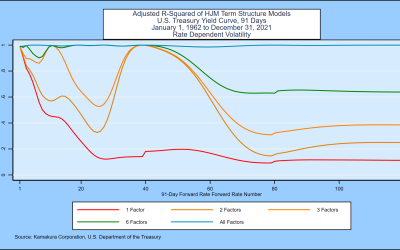

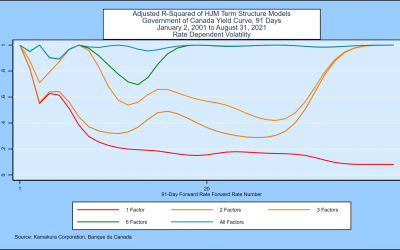

ABSTRACT This paper analyzes the number and the nature of factors driving the movements in the U.S. Treasury yield curve from...