Fat Tails, Transitory Inflation and the Credit Cycle

Kamakura Troubled Company Index Declines by 0.03% to 3.40%

Credit Quality Remains Strong at the 99th Percentile

NEW YORK, November 1, 2021: There is nothing scary about how credit quality ended the month – or is there?

The Kamakura Troubled Company Index® indicates that credit quality remained benign once again in October, standing at 3.40%, compared to 3.43% last month. Volatility was also low, with default probabilities ranging from 3.05% on October 8 to 3.49% on October 28. Over the past year, the index has declined by 14.96%. The low was set on August 12, at 2.06%. An increase in the index reflects declining credit quality, while a decrease reflects improving credit quality.

At the close of October, the percentage of companies with a default probability between 1% and 5% was 3.15%, an increase of 0.03% from the previous month. The percentage with a default probability between 5% and 10% was 0.21%, a decrease of 0.05%. Those with a default probability between 10% and 20% amounted to 0.04% of the total, representing no change; and those with a default probability of over 20% amounted to 0.00%, a decrease of 0.01% over the prior month. This level shows that worldwide corporate credit quality is at the 99th percentile for the period of 1990 to 2021, with 100 indicating “best conditions.”

Figure 1: Troubled Company Index — October 29, 2021

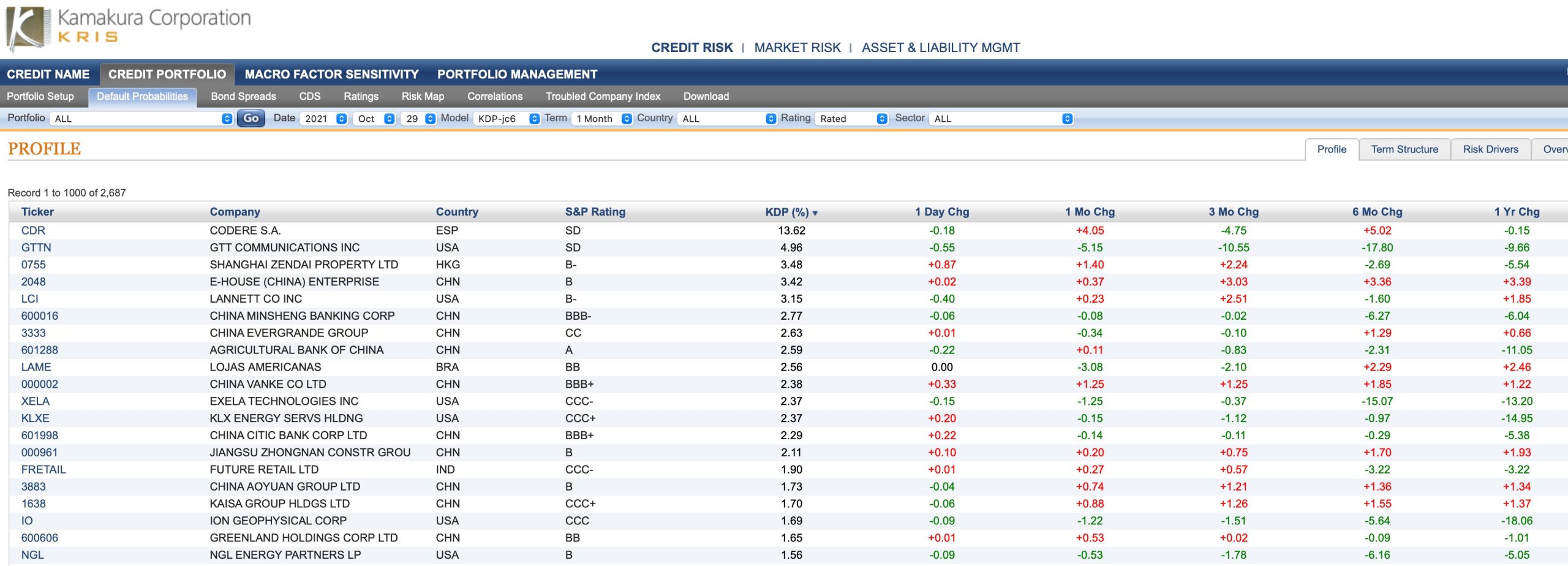

Among the 20 riskiest-rated firms listed in October, 11 were in China, with six in the U.S. and one each in Brazil, India and Spain. The riskiest-rated firm was Codere S.A. (BME:CDR), a Spanish consumer services and gaming company. The firm had a one-month KDP of 38.96%, up 5.63% from the previous month. There were four global defaults in the Kamakura coverage universe, three of which occurred in China and the other in the U.S.

Table 1: Riskiest-Rated Companies Based on 1-Month KDP – October 29, 2021

The Kamakura Expected Cumulative Default Rate, the only daily index of credit quality of rated-firms worldwide, shows the one-year rate up 0.05% at 0.80%, and the 10-year rate up 0.43% at 20.04%. The expected cumulative default rate for 10 years exceeds the 10-year rate in September, 2008 (the month that Lehman, AIG, FNMA, FHLMC and Washington Mutual failed).

Figure 2: Expected Cumulative Default Rate — October 29, 2021

Commentary

By Martin Zorn, President and Chief Operating Officer, Kamakura Corporation

I have often heard our Managing Director for Research, Professor Robert Jarrow, describe models simply and accurately as “abstract representations of a real-world setting.” Evaluating a model therefore requires testing its assumptions as well as its data.

In the real world, practitioners, especially those in quantitative finance, often blame “fat tails” for anomalies. Unlike a coin toss, in which the tails will be “thin” and predictable, markets and credit cycles tend to have extreme outcomes much more frequently than you would expect. The key question is how to predict them in advance. Debates about data issues, persistency and adjustments tend to justify the models and mask the impact of other dynamics at work, such as “group think” and clusters. Groups of members who think alike and interpret the data the same way may miss vital warning signs. Determining the right dynamic leading indicators, which change from cycle to cycle, becomes more difficult.

The current short-term environment is quite benign, with low levels of default, compression among spreads and ample liquidity. Using the U.S. as an example, Figure 3 below shows that the number of defaults through the end of the third quarter this year is down significantly from 2020.

Figure 3: Number of U.S. Defaults by Sector, Q1-Q3 2021 Versus Q1-Q3 2020

Low interest rates and a low level of corporate defaults outside of China and the energy sector continue to allow the markets and central banks to support companies with leveraged and fragile balance sheets. Markets seem to be focused on the one indicator of distress that has not occurred – an increase in global defaults, especially for leveraged companies.

But the indicator that worries me is continued pressure on the long end of the Kamakura Expected Cumulative default rate. The spread between short and long-term default rates is not a normal part of the model or data history. What are its drivers?

As I read the third quarter banking releases, I noticed that banks, driven by low short-term default risks, continue to release reserves. That raises a scary question: Have central bank policies created a generation of “zombie” firms that would have failed if not for fiscal and monetary policies of easy and free money?

More than ever, I am looking to the bond market, rather than the equity markets, to be the first to react to a rise in defaults created by an economic slowdown, a rise in interest rates, a decline in liquidity, or some combination of these factors. Our central banks will be playing catch-up, and I question whether they have the will to act or to admit their role in creating the next crisis.

Kamakura CEO Dr. Donald van Deventer addresses the current situation in his daily blog, Corporate Bond Investor, which examines attribution of risks as they relate to changes in bond prices. Table 2 below shows the one-month attribution as of October 29, 2021.

Table 2: Bond Performance Attribution – October 29, 2021

Dr. van Deventer’s analysis provides insights into whether systemic risk (as measured by Treasury-related changes) or company-specific risks (as measured by credit-related changes) are driving the price changes. The bond market has a strong track record for providing insight about future economic growth.

About the Troubled Company Index

The Kamakura Troubled Company Index® measures the percentage of 40,500 public firms in 76 countries that have an annualized one- month default risk of over one percent. The average index value since January 1990 is 14.37%. Since November 2015, the Kamakura index has used the annualized one-month default probability produced by the KRIS version 6.0 Jarrow-Chava reduced form default probability model, a formula that bases default predictions on a sophisticated combination of financial ratios, stock price history, and macro-economic factors.

The KRIS version 6.0 models were developed using a data base of more than 2.2 million observations and more than 2,600 corporate failures. A complete technical guide, including full model test results and parameters, is provided to subscribers. The KRIS service also includes a wide array of other default probability models that can be seamlessly loaded into Kamakura’s state-of-the-art enterprise risk management software engine, the Kamakura Risk Manager. Available models include the non-public-firm default model, the commercial real estate model, the U.S. bank model, and the sovereign model. Related data includes credit default swap trading volume by reference name, market implied credit spreads, and prices on all traded corporate bonds traded in the U.S. market. Macro factor parameter subscriptions include Heath, Jarrow, and Morton term structure models for government securities in the U.S., Germany, the UK, Canada, Spain, Sweden, Australia, Japan, Thailand, and Singapore. All parameters are derived in a no-arbitrage manner consistent with seminal papers by Heath, Jarrow, and Morton, as well as Amin and Jarrow. A KRIS Macro Factor Scenario Service subscription includes both risk neutral and “real world” empirical scenarios for interest rates and macro factors.

The version 6.0 model was estimated over the period from 1990 to May 2014 and includes the insights of the entirety of the recent credit crisis. The 76 countries currently covered by the index are: Argentina, Australia, Austria, Bahrain, Bangladesh, Belgium, Belize, Botswana, Brazil, Bulgaria, Canada, Chile, China, Colombia, Croatia, Cyprus, Czech Republic, Denmark, Egypt, Estonia, Finland, France, Germany, Ghana, Greece, Hungary, Hong Kong, Iceland, India, Indonesia, Ireland, Israel, Italy, Japan, Jordan, Kenya, Kuwait, Luxembourg, Malaysia, Malta, Mauritius, Mexico, Nigeria, the Netherlands, New Zealand, Norway, Oman, Pakistan, Peru, the Philippines, Poland, Portugal, Qatar, Romania, Russia, Saudi Arabia, Serbia, Singapore, Slovakia, Slovenia, South Africa, South Korea, Spain, Sri Lanka, Sweden, Switzerland, Tanzania, Taiwan, Thailand, Turkey, the United Arab Emirates, Uganda, the UK, the U.S., Vietnam and Zimbabwe.

About Kamakura Corporation

Founded in 1990, Honolulu-based Kamakura Corporation is a leading provider of risk management information, processing, and software. Kamakura was recognized as a category leader in the Chartis Report, Technology Solutions for Credit Risk 2.0 2018. Kamakura was named to the World Finance 100 by the editor and readers of World Finance magazine in 2017, 2016 and 2012. In 2010, Kamakura was the only vendor to win two Credit Magazine innovation awards., Kamakura Risk Manager, first sold commercially in 1993 and now in version 10.1, is the first enterprise risk management system for users focused on credit risk, asset and liability management, market risk, stress testing, liquidity risk, counterparty credit risk, and capital allocation from a single software solution. The KRIS public firm default service was launched in 2002. The KRIS sovereign default service, the world’s first, was launched in 2008, and the KRIS non-public firm default service was offered beginning in 2011. Kamakura added its U.S. Bank default probability service in 2014.

Kamakura has served more than 330 clients with assets ranging in size from $1.5 billion to $7.0 trillion. Current clients have a combined “total assets” or “assets under management” in excess of $34 trillion. Its risk management products are currently used in 47 countries, including the United States, Canada, Germany, the Netherlands, France, Austria, Switzerland, the United Kingdom, Russia, Ukraine, South Africa, Australia, China, Hong Kong, India, Indonesia, Japan, Korea, Malaysia, Singapore, Sri Lanka, Taiwan, Thailand, Vietnam, and many other countries in Asia, Europe and the Middle East.

To follow risk commentary by Kamakura on a daily basis, please follow:

Kamakura CEO, Dr. Donald van Deventer (www.twitter.com/dvandeventer)

Kamakura President, Martin Zorn (www.twitter.com/riskmgrhi)

Kamakura’s official twitter account (www.twitter.com/KamakuraCo).

For more information, please contact:

Kamakura Corporation

2222 Kalakaua Avenue, Suite 1400, Honolulu, Hawaii 96815

Telephone: 1-808-791-9888

Facsimile: 1-808-791-9898

Information: info@kamakuraco.com

Web site: www.kamakuraco.com