NEW YORK: November 4,2024: Economic headlines—including those about employment, inflation, and the stock market–have been generally upbeat and positive lately. The S&P 500 has set 47 record highs thus far in 2024. Household net worth marked another all-time high in 2024:Q2 at $163.8T – an increase of $46.6T or 40% from the pre-pandemic levels (2019:Q4). During the same time the value of assets grew by 38%, well outpacing the liabilities growth of 25%. To put this in perspective, the increase in the household net worth eclipsed the total value of the US federal debt which stood at $35.95T as of end of October. This is a remarkable display of the strength of the US economy and the strength of the consumer, who is responsible for roughly two-thirds of the GDP.

But beneath the surface lie variances that are concerning, especially as they affect the working and middle classes. This trend has been underway for some time, but the impact of inflation and the growing divide between home and stock ownership or the lack of it have exacerbated the gap. The cumulative rate of inflation from pre-pandemic to middle of 2024 was 21%. When adjusted for inflation, the household net worth increased by 15% from the pre-pandemic levels – a pace that was marginally slower than what transpired in the beginning of this century prior to the pandemic.

Figure 1: Total Assets Net of Mortgage Debt ($T in Inflation-Adjusted 2024:Q4 Dollars)

Source: SAS Institute; The Board of Governors of the Federal Reserve System, Financial Accounts of the United States – Z.1

Table 1: Change in Real Value of Total Assets Net of Mortgage Debt

Source: SAS Institute; The Board of Governors of the Federal Reserve System, Financial Accounts of the United States – Z.1

When total household assets are deconstructed into their underlying components as it is shown in the Figure 1 and Table 1 above, a more nuanced picture emerges. Most of the gains since the beginning of pandemic came from the value of real estate net of mortgage debt and from direct investments, where vast majority of the gains were attributable to equities. At the same time, as defined benefit plans were being phased out and individual’s savings into the defined contribution plans have not kept pace, the value of “DB + Indirect Investments” category have declined by 6% in real terms. While there are several factors that are impacting this trend, the decrease in retirement safety net is the main theme behind the decline.

While the stock ownership by Americans has been increasing and now stands at the highest level since the Global Financial Crisis, the ownership of stock also increases the divide between those who benefit from equity and those who do not. The same is true for homeownership, which provides owners with equity and price appreciation, while renters not only miss out on these benefits, but often must contend with higher lease payments as well.

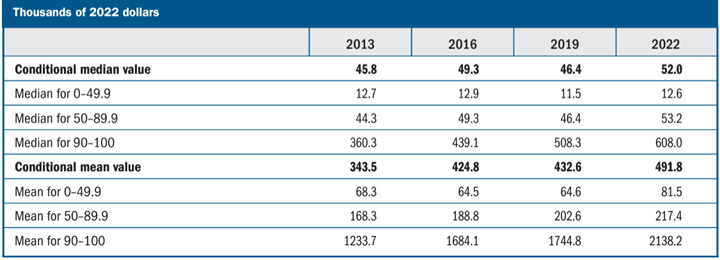

Once again, the headline statistic that well over half of the US households are stockowners is a bit misleading. Majority of that share is driven by indirect holdings in the retirement accounts – the segment of net assets that declined post-pandemic on inflation-adjusted basis. When considering direct stock ownership only (i.e., the area that experienced some of the largest asset growth in recent years), the share of participation falls to 21% of the households[1]. Furthermore, when considering the mean and median value of the holdings by income group, the distribution is extremely skewed towards the top decile (Table 2). In 2022, the mean value of stock holdings of the top income decile was almost 10x the value of 50th-89th percentile group and 26x the average value of the bottom half. Note that these statistics are based on the conditional mean value, meaning that they are calculated only from families that do own stocks. When multiplied by the stock ownership rates (Chart 2) the divide becomes even more stark.

Figure 2: Stock Ownership (Direct and Indirect) by Income Group

Source: Survey of Consumer Finances – Board of Governors of the Federal Reserve System

Table 2: Median and Mean Levels of Directly and Indirectly Held Stock by Income Group

Source: Survey of Consumer Finances – Board of Governors of the Federal Reserve System

What about the real estate, which as the other major area of asset value growth? According to the Urban Institute, more than 70% of people aged 35-44 owned a home in 1980 but by 2018 less than 60% of people in that age group had bought their own home. Four in 10 middle class households are now burdened by rent costs, which are up 20% from 2019. Housing is now unaffordable for a record half of U.S. renters. (Cost- burdened households are generally defined as those paying 30% or more of pretax income on rent or housing.)

Figure 3: Rental Inflation

Viewed together, these trends explain the increase in consumer delinquencies, especially for credit card and auto loans. Last month we pointed out the non-current and charge-off rates noted in the most recent FDIC banking profile. Figure 4 shows the updated delinquency trends. Auto delinquency rates have been rising the most precipitously and have been above pre-pandemic levels for some time. The pain felt by the middle class impacts corporations differently, based on their products and target markets. As delinquencies and charge- offs rise, we must carefully examine the overall availability of credit, as it is normal for providers to proactively reduce their exposure. Furthermore, the rapidly growing BNPL (buy now pay later) market has yet to be tested during the major credit cycle. Diminishing credit availability can also increase pressure on commercial loans and lead to defaults.

Figure 4: Non-Current Loan Rate and Quarterly Net Charge-off Rate

The contemporaneous credit conditions report notes a large jump in the 10- year expected cumulative default rate, from 7.41% at the end of September to 8.91% at the end of last month. The expected cumulative default curve also implies that we will see the 1-year default rate rise from 52 basis points to 0.98% one year from now and 1.17% two years from now. While these charge-off rates remain low by recessionary standards, they are high by recent standards and should serve as a warning sign for investment managers to be nimble, on-guard, and proactive in making portfolio decisions.

Contemporaneous Credit Conditions

The Kamakura Troubled Company Index® closed the month at 9.22%, up 0.34% from the prior month. The index measures the percentage of 42,500 public firms worldwide with an annualized one-month default probability of over 1%. An increase in the index reflects declining credit quality, while a decrease reflects improving credit quality.

At the end of October, the percentage of companies with a default probability between 1% and 5% was 6.76%. The percentage with a default probability between 5% and 10% was 1.31%. Those with a default probability between 10% and 20% amounted to 0.84% of the total; and those with a default probability of over 20% amounted to 0.31%. For the month, short-term default probabilities ranged from a low of 8.82% on October 4 to a high of 9.40% on October 25. There were 16 defaults in our coverage universe, with six in the United States, two each in China and Sweden and one each in France, Germany, Italy, India, Switzerland and the UK.

Figure 5: Troubled Company Index®, October 31, 2024

At the end of October, the riskiest 1% of rated public firms within the coverage universe as measured by 1-month default probability included 9 companies in the U.S. and one each in Brazil, Canada and France. The riskiest firm continued to be the Container Store Group (NYSE:TCS), with a one-month KDP of 49.28%, down 2.14% for the month. Interestingly Figure 6 shows that the 1-year KDP for the firm remains higher than the ratings implied default rate despite multiple downgrades.

Table 3: Riskiest Rated Companies Based on 1-month KDP, October 31, 2024

Figure 6: 1-Year KDP Container Store Group

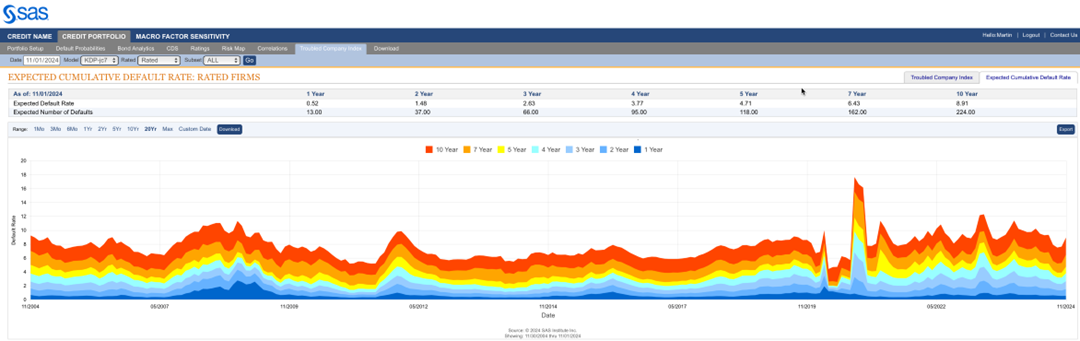

The Kamakura Expected Cumulative Default Rate, the only daily index of credit quality of rated firms worldwide, shows the one-year rate of 0.52% up 0.01% from the prior month, with the 10-year rate up 1.49% at 8.90%.

Figure 7: Expected Cumulative Default Rates, November 1, 2024

About the Troubled Company Index

The Kamakura Troubled Company Index® measures the percentage of 42,500 public firms in 76 countries that have an annualized one-month default risk of over one percent. The average index value since January 1990 is 14.08%. Since July 2022, the index has used the annualized one-month default probability produced by the KRIS version 7.0 Jarrow-Chava reduced form default probability model, a formula that bases default predictions on a sophisticated combination of financial ratios, stock price history, and macro-economic factors.

The KRIS version 7.0 models were developed using a data base of more than 4 million observations and more than 4,000 corporate failures. A complete technical guide, including full model test results and key parameters, is provided to subscribers. Available models include the non-public-firm default model, the U.S. bank model, and the sovereign model.

The version 7.0 model was estimated over the period from 1990, through the Great Recession and ending in February 2022. The 76 countries currently covered by the index are Argentina, Australia, Austria, Bahrain, Bangladesh, Belgium, Belize, Botswana, Brazil, Bulgaria, Canada, Chile, China, Colombia, Croatia, Cyprus, Czech Republic, Denmark, Egypt, Estonia, Finland, France, Germany, Ghana, Greece, Hungary, Hong Kong, Iceland, India, Indonesia, Ireland, Israel, Italy, Japan, Jordan, Kenya, Kuwait, Luxembourg, Malaysia, Malta, Mauritius, Mexico, Nigeria, the Netherlands, New Zealand, Norway, Oman, Pakistan, Peru, the Philippines, Poland, Portugal, Qatar, Romania, Russia, Saudi Arabia, Serbia, Singapore, Slovakia, Slovenia, South Africa, South Korea, Spain, Sri Lanka, Sweden, Switzerland, Tanzania, Taiwan, Thailand, Turkey, the United Arab Emirates, Uganda, the UK, the U.S., Vietnam and Zimbabwe.

About SAS

SAS is the leader in analytics. Through innovative software and services, SAS empowers and inspires customers around the world to transform data into intelligence. SAS gives you THE POWER TO KNOW®.

Editorial contacts:

- Martin Zorn – Martin.Zorn@sas.com

- Stas Melnikov – Stas.Melnikov@sas.com

[1] Survey of Consumer Finances – Board of Governors of the Federal Reserve System. https://www.federalreserve.gov/econres/scfindex.htm