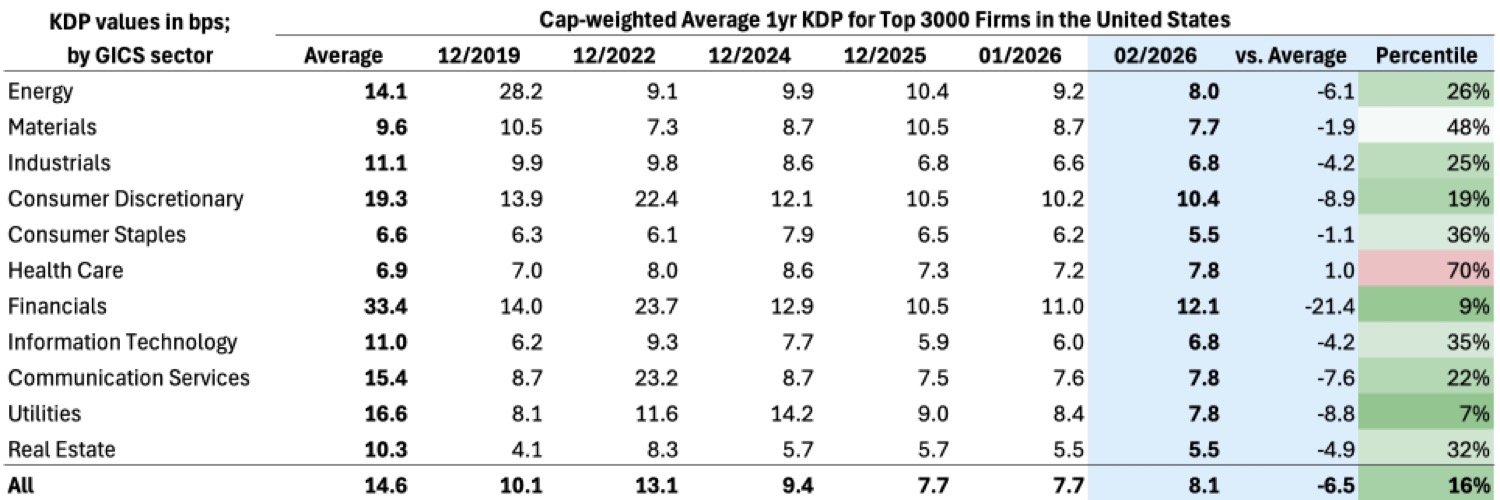

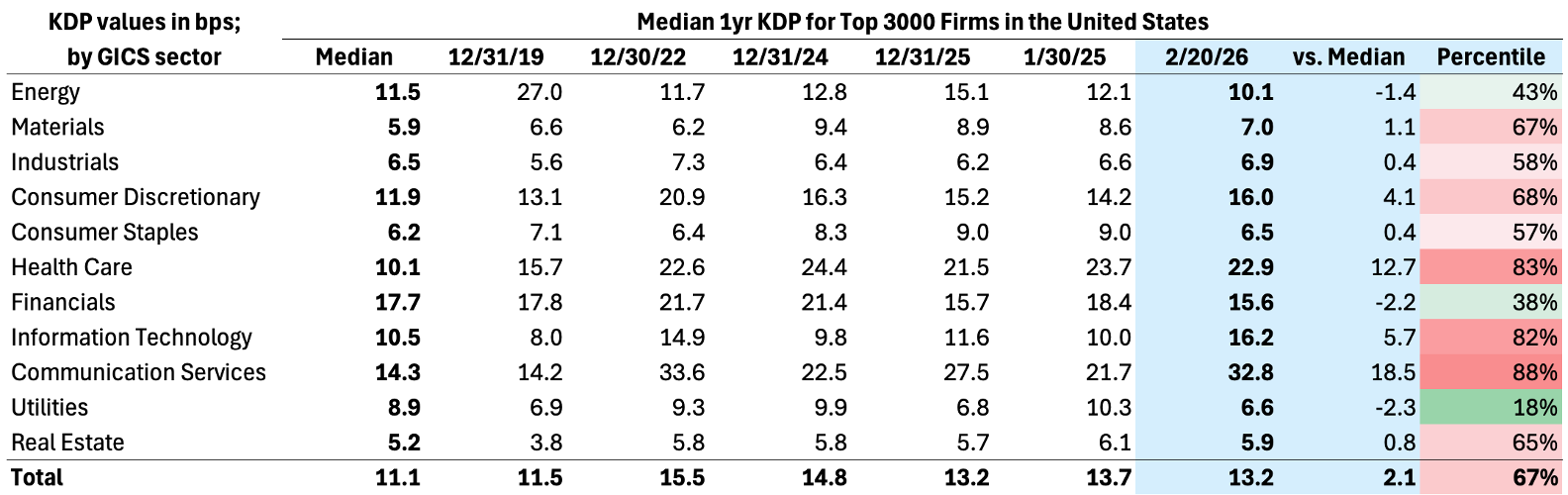

February saw a modest widening in public credit spreads: the ICE BofA U.S. Corporate (IG) OAS widened from 75 bps at January month-end to 86 bps at February month-end, while the ICE BofA U.S. High Yield OAS widened from 288 bps to 312 bps. Equity markets were little changed with S&P 500 dropping -0.9% and Russell 2000 gaining 0.7%. Within KRIS, market cap-weighted default probabilities were mostly unchanged. At the same time median (count-weighted) default probabilities increased, most visibly in the longer-dated part of the term structure. The distributional message remains consistent with prior months: index-level calm can coexist with a weaker “typical” issuer. At a sector level[1], median 1yr KDPs showed notable increases in Information Technology and Communications Services sectors. On a market cap-weighted average basis, the largest increases were in Financials, Information Technology and Health Care. IT sector, stressed by the concerns about AI-driven disruption and spiraling capex costs, was the only sector that had an increase in both median and weighted average metrics.

At the same time, February’s backdrop included renewed stress signals in private credit. Blue Owl permanently halted redemptions in OBDC II and Apollo-managed MFIC private credit fund cutting dividend and marking down portfolio to name a few. These are liquidity/valuation credibility events in vehicles sold on ‘steady NAV + steady income’ narratives. Taken together, February’s story was less about a generalized spread shock and more about credibility as a fault line: the aggregate of conditions that allow lenders to underwrite cash flows with confidence. Specifically, clean financial reporting, dependable controls, transparent disclosure, stable governance, and predictable access to liquidity. When credibility weakens, credit does not typically reprice smoothly; it reprices in jumps.

Last month’s newsletter[2] highlighted a structural fragility in Information Technology, visible in KRIS as one of the widest gaps between median KDP and cap-weighted KDP. That is an important metric: it implies that index-level stability is being propped up by a small set of very large “winner” names, while the typical IT firm is meaningfully weaker. That dispersion matters because it changes how stress propagates:

- In a sector with market cap concentrated in a few very large firms[3], the index can stay calm (and Alphabet can still issue 100yr bonds[4] at ~120bps spread over gitls!) while the median firm deteriorates.

- When the median firm deteriorates, idiosyncratic events have a larger probability of occurring somewhere in the cohort.

- When the event is a credibility event (controls, accounting, guidance integrity), the repricing tends to be discontinuous.

February delivered a clear example of how that fragility can convert into abrupt market moves: Kyndryl Holdings (KD). Kyndryl is a large IT infrastructure services provider (spinoff of IBM’s managed infrastructure services business) and runs mission-critical “keep the lights on” work: hybrid infrastructure operations, mainframe/distributed hosting, workplace services, network, and related managed services for large enterprises[5]. The business is operationally sticky but structurally exposed to execution risk and, critically, credibility risk when reporting and controls come into question.

On Feb 9, 2026, Kyndryl reported fiscal Q3 results that included sharp downward revisions to its full-year outlook (revenue, pretax income, free cash flow), alongside notable executive changes (CFO and general counsel abrupt departures). The same day, the company disclosed its audit committee began reviewing cash management practices, disclosures and internal controls after voluntary document requests from the SEC’s enforcement division; it also delayed its quarterly filing and anticipated reporting material weaknesses. The company then filed its delayed 10-Q on Feb 17, explicitly disclosing material weaknesses in internal control over financial reporting and outlining remediation steps.

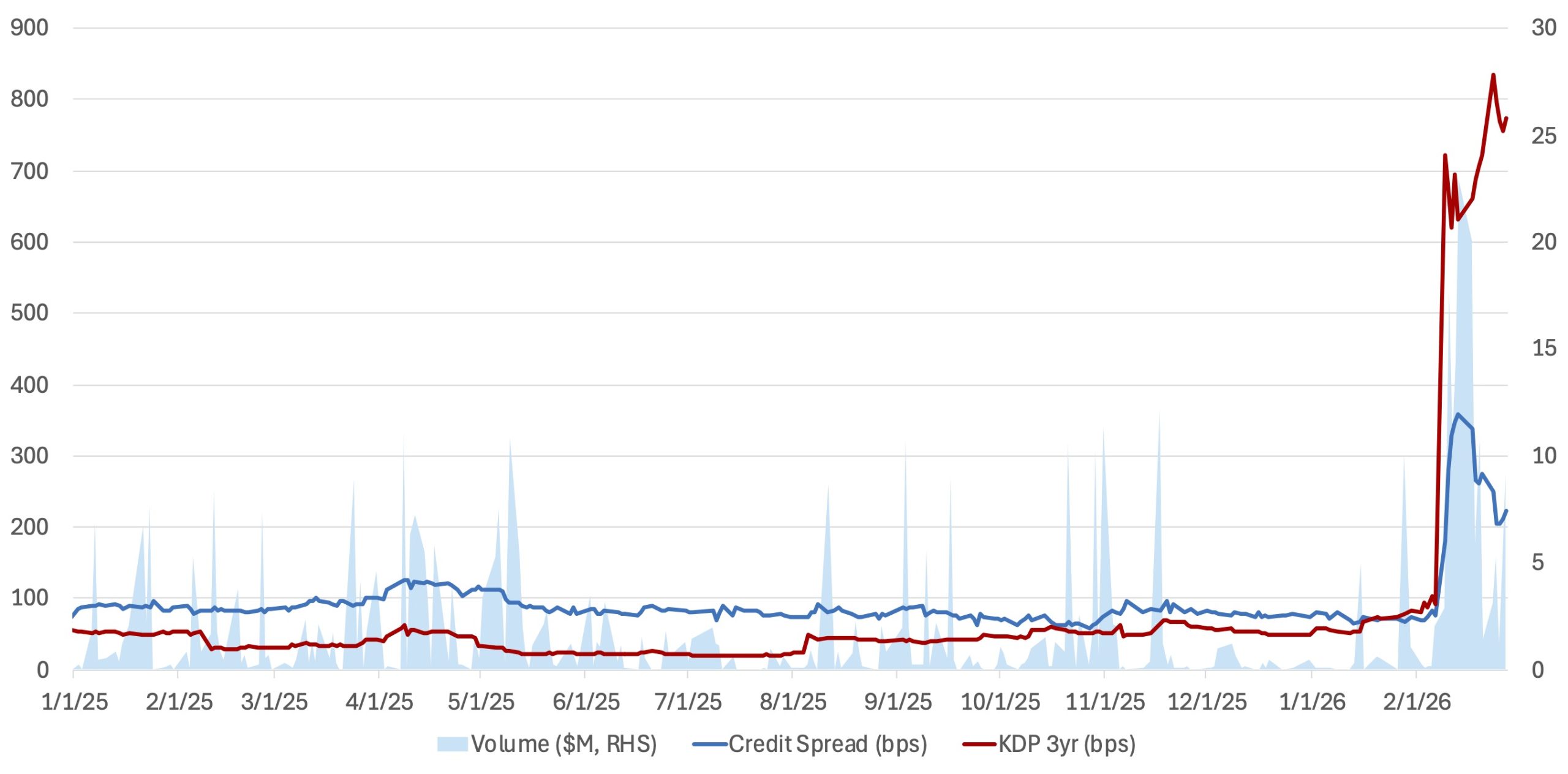

In the month leading up to the event, credit spreads (using 2.7% coupon bond due in 2028 as an illustration) were unchanged at 77bps, indicating a minimal credit risk. During the same period, 3yr KDP increased from 48bps to 91bps (almost doubled). During the week following the announcement, credit spreads widened by 282bps while 3yr KDP increased by 540bps. By the end of February, credit spreads came down to 200bps range (well below where HY index ended the month), while KDPs continue to climb. Such divergence warrants caution going forward as bond pricing may not be adequately compensating for credit risk in this situation.

Implication going forward: February reinforced that this cycle’s fragility is not primarily about the broad spread beta; it is about issuer-level fundamentals and credibility in high-dispersion sectors. In Information Technology, where the median issuer remains significantly weaker than the cap-weighted index, the probability of discontinuous single-name moves is high, and the repricing can be sudden. Other sectors that warrant close monitoring are Communication Services and Healthcare.

Figure 1: KDP and Credit Spreads for Kyndryl Holdings (ISIN: US50155QAK67)

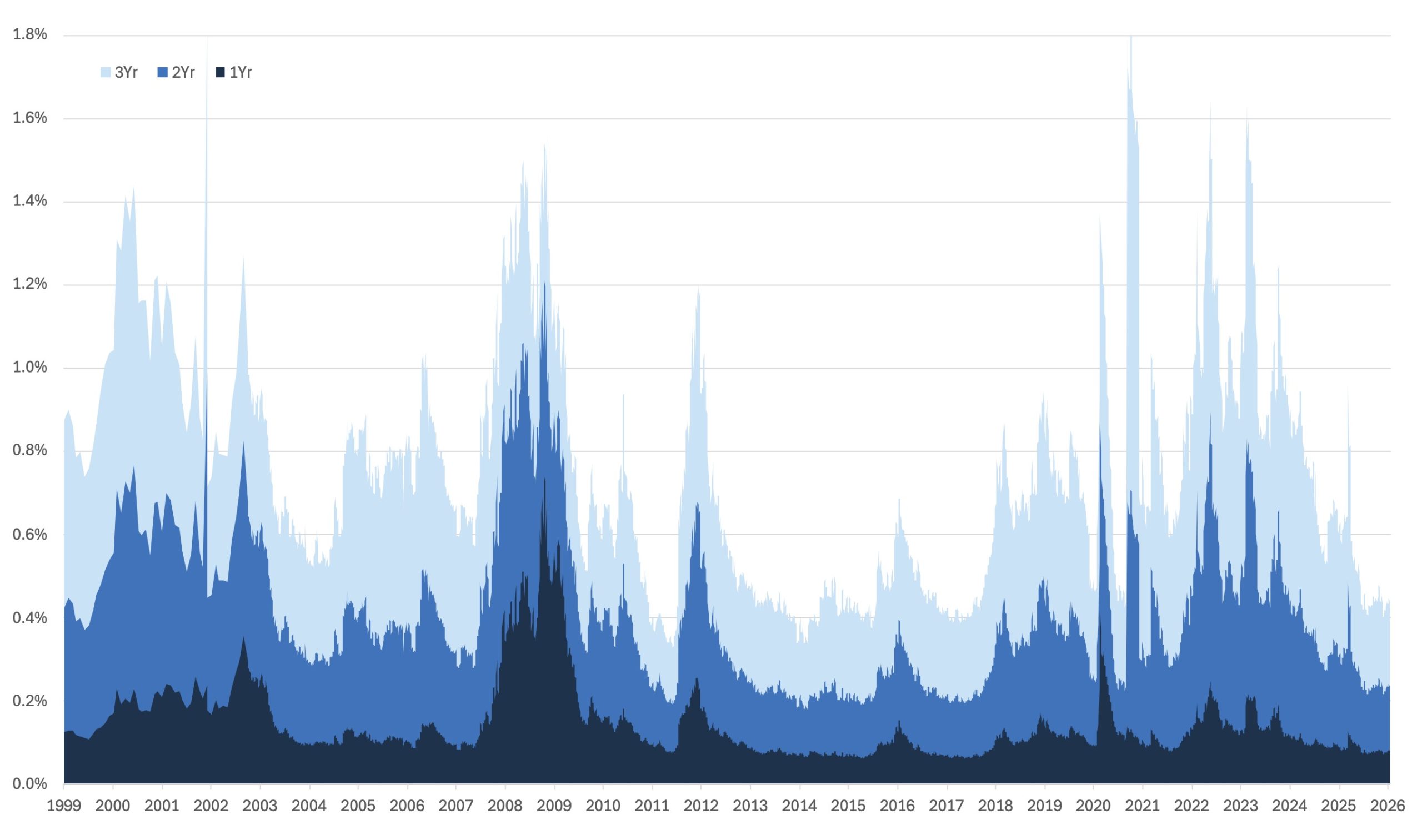

Figure 2: Market Cap-Weighted Cumulative Default Probability – Top 3000 Companies in the United States

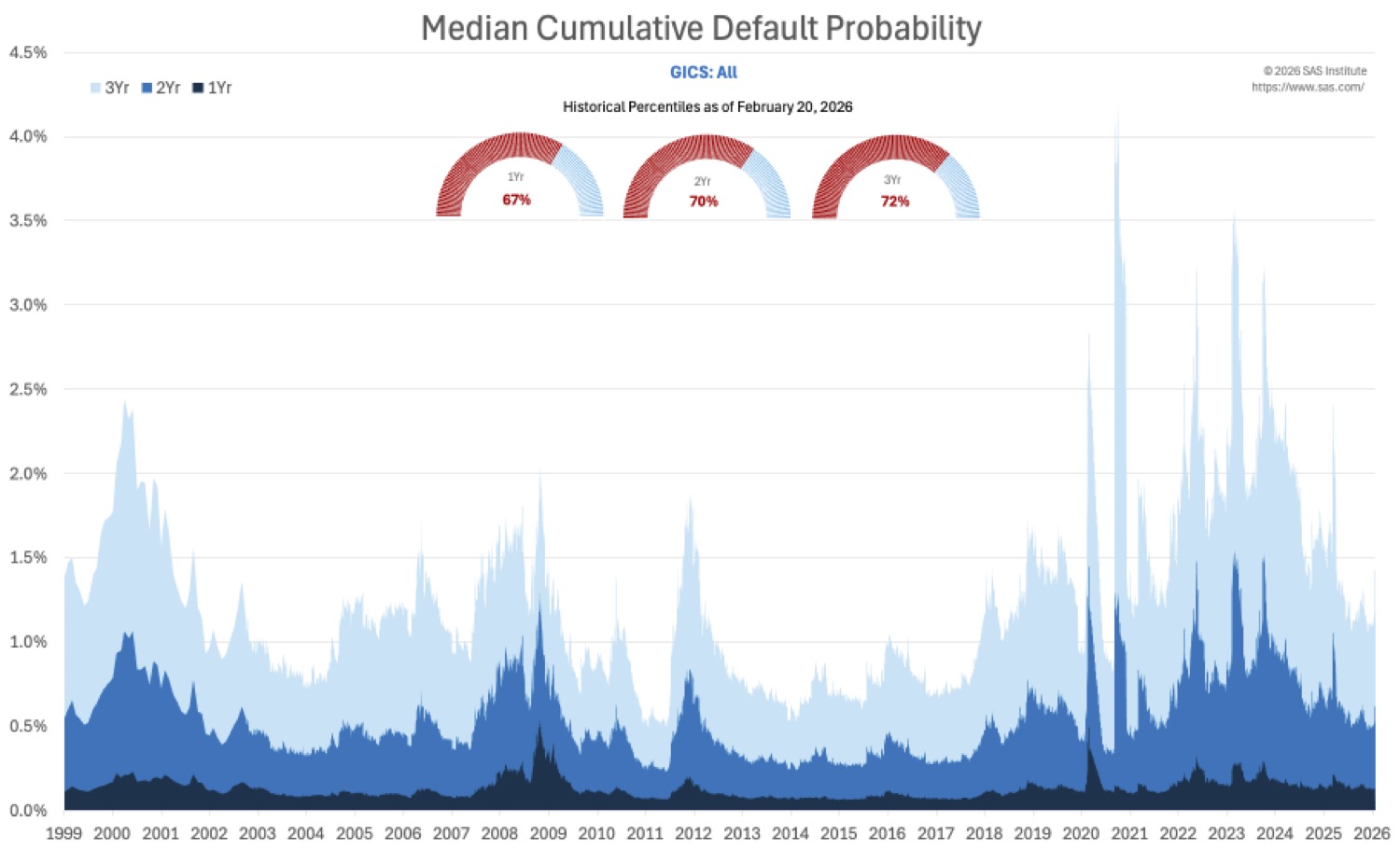

Figure 3: Median Cumulative Default Probability – Top 3000 Companies in the United States

Table 1: Market Cap-Weighted Average 1-year Default Probability (Top 3000 Firms in the United States)

Table 2: Median 1-year Default Probability (Top 3000 Firms in the United States)

Why KRIS KDP matters now. Market prices can remain calm even as underlying risk concentrates, making model-based, issuer-level signals essential. KRIS default probabilities provide daily, issuer-level signals that make the bifurcation visible – pinpointing names where refinancing pressure, equity-vol shocks, or weakening coverage are rising even when spreads don’t budge. Used alongside market spreads and fundamentals, KDPs help identify issues not yet priced, providing actionable early warnings.

Appendix

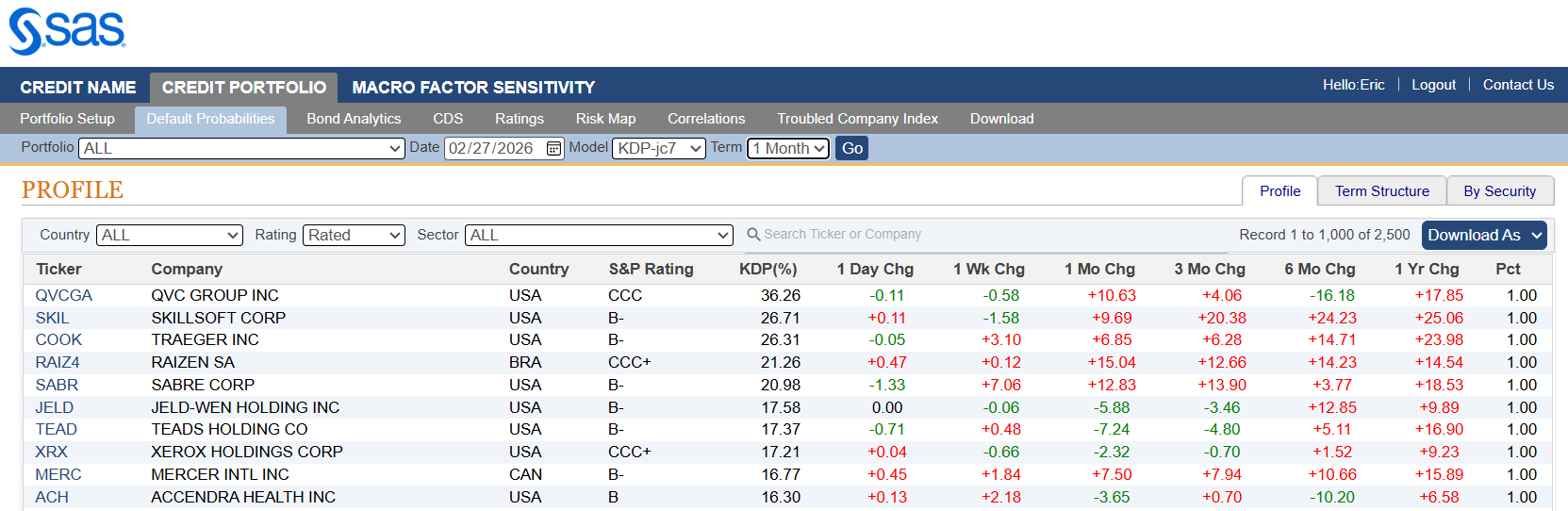

Table 3: Riskiest Rated Companies Based on 1-month KDP, February 27th, 2026

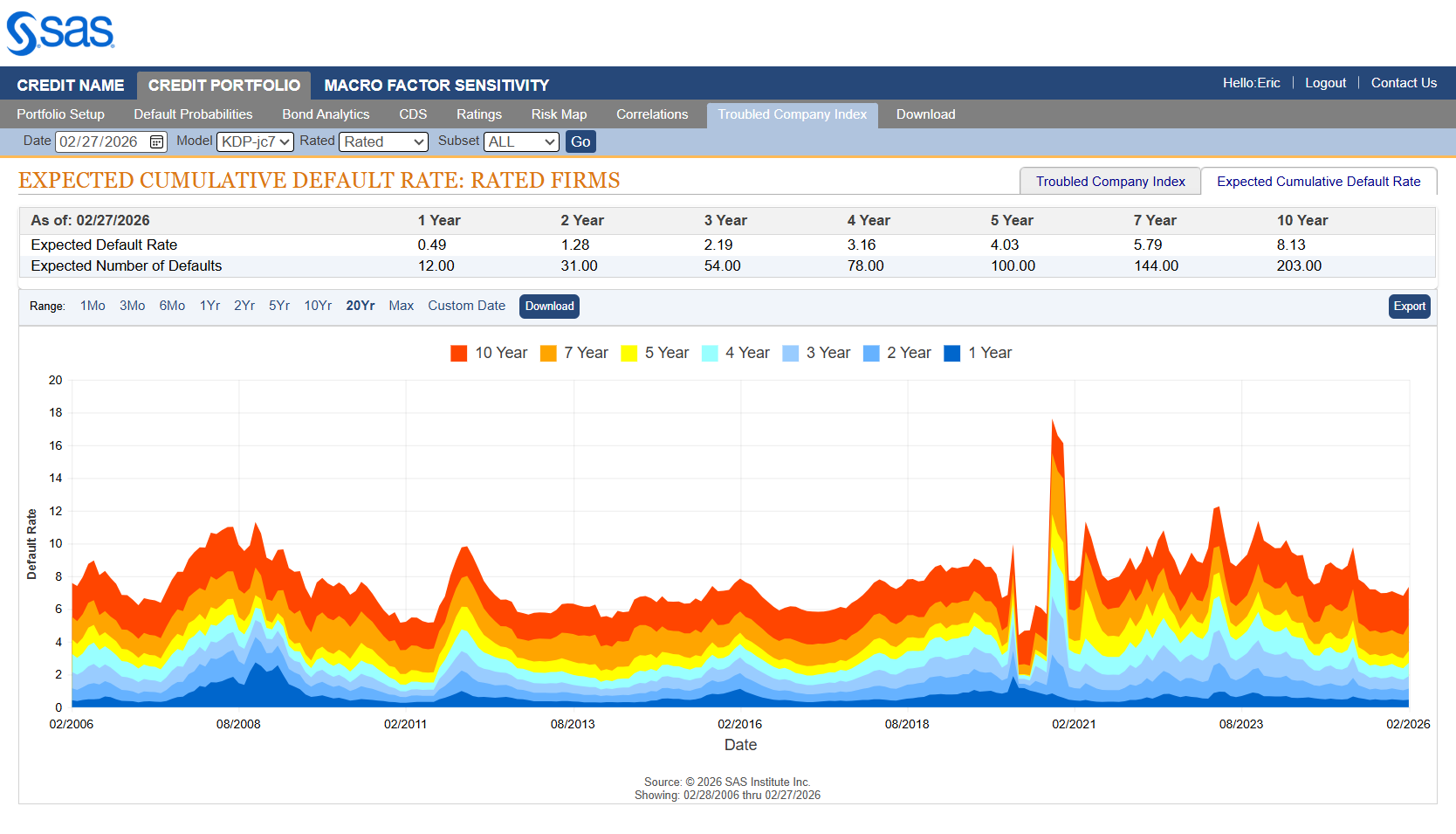

Figure 4: Expected Cumulative Default Rates, February 27th, 2026

About SAS

SAS is the leader in analytics. Through innovative software and services, SAS empowers and inspires customers around the world to transform data into intelligence. SAS gives you THE POWER TO KNOW®.

Editorial contact: Stas Melnikov – stas.melnikov@sas.com

[1] Analysis based on largest 3000 firms by market capitalization in the United States. The top 3000 ranks are calculated on a daily basis.

[2] https://www.kamakuraco.com/divergence-in-credit-conditions-index-level-resilience-vs-typical-firm-strain/

[3] https://www.kamakuraco.com/the-narrowing-definition-of-winner/

[4] https://www.reuters.com/business/alphabet-sells-bonds-worth-20-billion-fund-ai-spending-2026-02-10/

[5] https://www.cio.com/article/189224/what-is-kyndryl-ibms-managed-infrastructure-services-spin-off-explained.htm