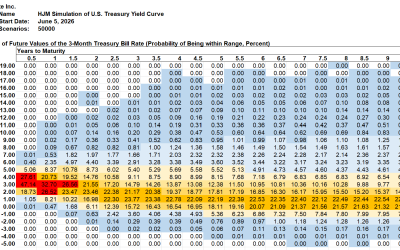

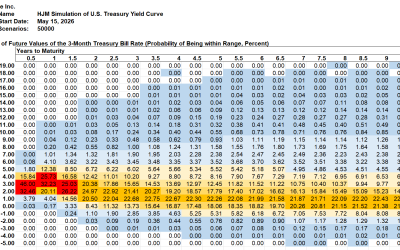

Summary The most likely range for 3-month bill yields in 10 years remained at the 1% to 2% range this week. The probability of...

Summary The most likely range for 3-month bill yields in 10 years remained at the 1% to 2% range this week. The probability of...

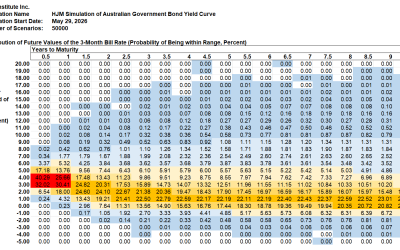

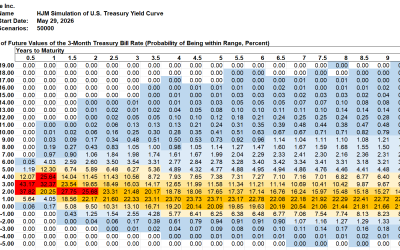

The Heath, Jarrow and Morton [1992] framework for simulation and valuation using risk-free interest rates has been called “the...

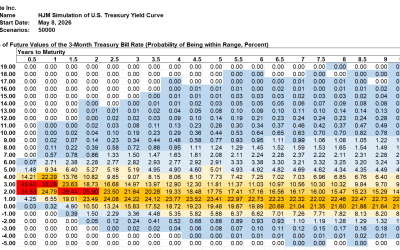

Summary The most likely range for 3-month bill yields in 10 years remained at the 1% to 2% range this week. The probability of...

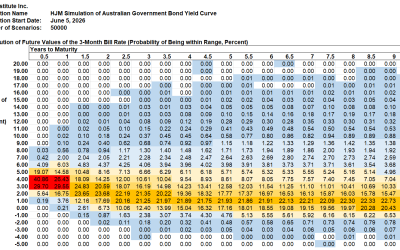

The Heath, Jarrow and Morton [1992] framework for simulation and valuation using risk-free interest rates has been called “the...

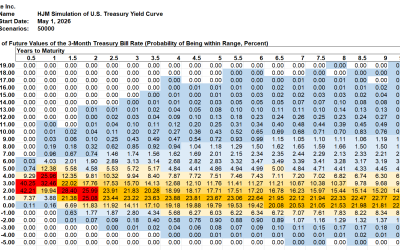

Summary The most likely range for 3-month bill yields in 10 years remained at the 1% to 2% range this week. The probability of...

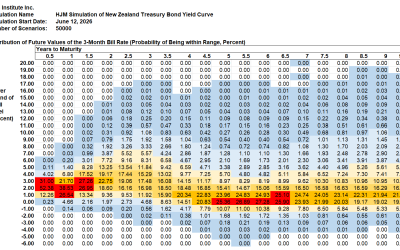

The Heath, Jarrow and Morton [1992] framework for simulation and valuation using risk-free interest rates has been called “the...

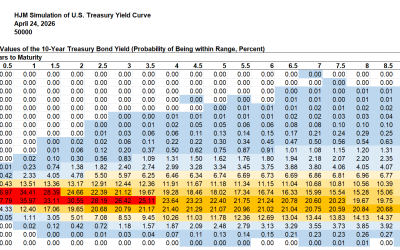

Summary The most likely range for 3-month bill yields in 10 years remained at the 1% to 2% range this week. The probability of...

Summary The most likely range for 3-month bill yields in 10 years remained at the 1% to 2% range this week. The probability of...

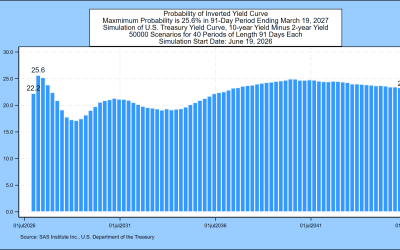

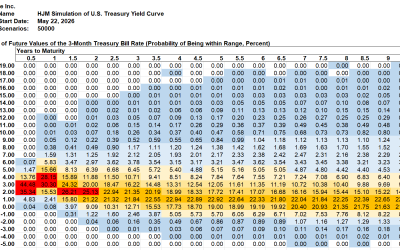

Summary After a short-term rise, the most likely range for 3-month bill yields in 10 years remained at the 1% to 2% range this...

Summary The most likely range for 3-month bill yields in 10 years remained at the 1% to 2% range this week. The probability of...

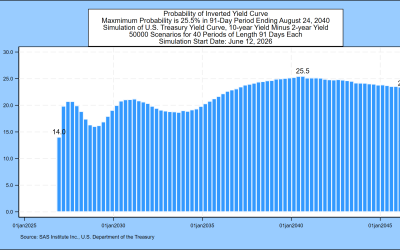

Summary The most likely range for 3-month bill yields in 10 years remained at the 1% to 2% range this week. The probability of...

Summary The most likely range for 3-month bill yields in 10 years remained at the 1% to 2% range this week. The probability of...