The streak of negative 2-year/10-year Treasury spreads has now reached 287 trading days, 9 trading days longer than the third...

The streak of negative 2-year/10-year Treasury spreads has now reached 287 trading days, 9 trading days longer than the third...

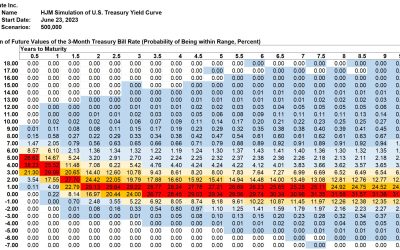

The streak of negative 2-year/10-year Treasury spreads has now reached 277 trading days, 1 trading day from the second longest...

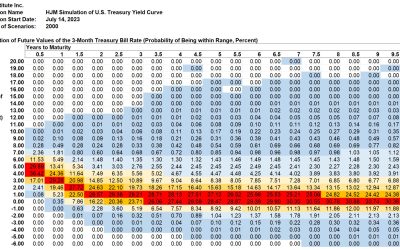

The current Treasury yield curve implies a long-run peak of 1-month Treasury forward rates at 5.28%, up 0.20% from last week....

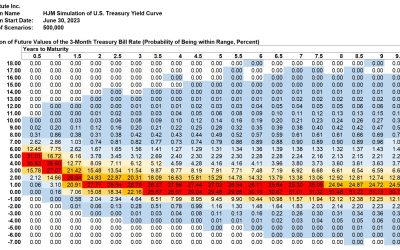

The current Treasury yield curve implies a long-run peak of 1-month Treasury forward rates at 5.08%, up 0.15% from last week....

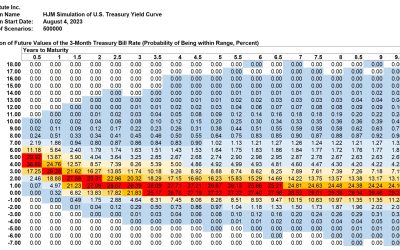

Abstract The size of the term premium embedded in the current U.S. Treasury yield curve has been a major focus of research by...

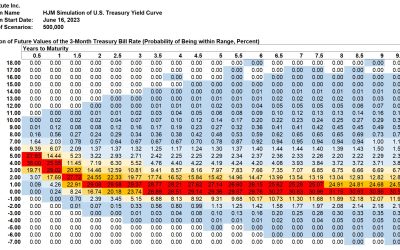

The streak of negative 2-year/10-year Treasury spreads has now reached 262 trading days, 16 trading days from the second longest...

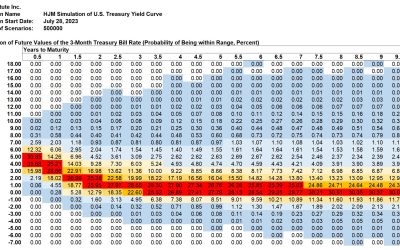

This week’s U.S. Treasury yield curve shifts reversed most of the increase from the prior week. The long-term peak in 1-month...

This week’s shift in the U.S. Treasury yield drove the negative 2-year/10-year Treasury spread to a negative 106 basis points....

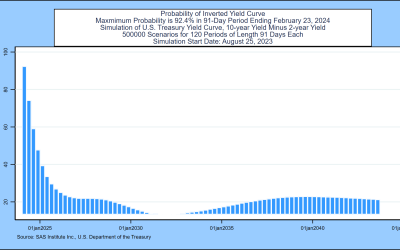

This week’s simulation shows that the current negative 2-year/10-year Treasury yield spread is a near certainty to persist at...

This week’s simulation shows an interest rate outlook very similar to last week, a pause after the Fed’s pause in rate hikes....

The resolution of the Treasury debt cap crisis has resulted in a significant downward shift in the U.S. Treasury forward rate...

As of Friday, the current streak of trading days with a negative 2-year/10-year Treasury spread has reached 225 days, the third...