As of Friday, the current streak of trading days with a negative 2-year/10-year Treasury spread has reached 220 days, tied with...

As of Friday, the current streak of trading days with a negative 2-year/10-year Treasury spread has reached 220 days, tied with...

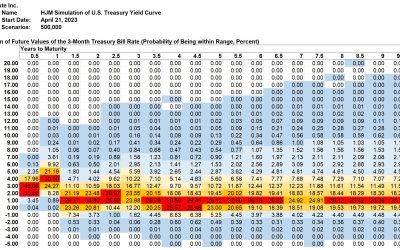

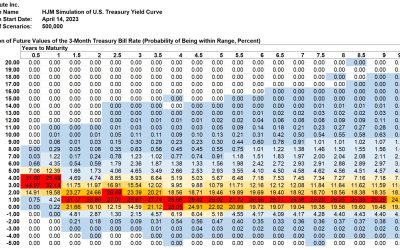

Both implied forward Treasury 1-month bill rates and simulated 3-month bill rates show a sharp drop in the near term, especially...

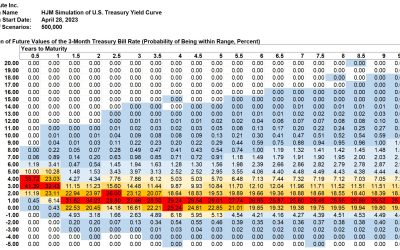

Both implied forward Treasury 1-month bill rates and simulated 3-month bill rates show much less volatility this week. A sharp...

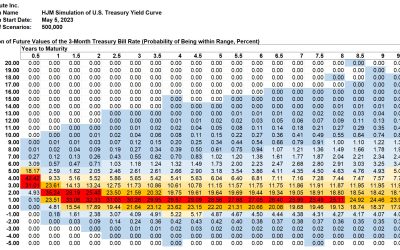

Both implied forward Treasury 1-month bill rates and simulated 3-month bill rates show high volatility and a sharp downshift,...

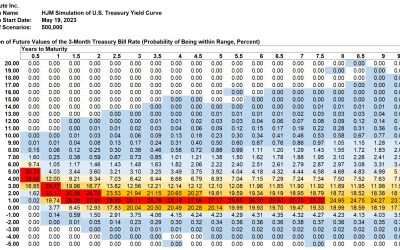

Both implied forward Treasury 1-month bill rates and simulated 3-month bill rates show high volatility and a sharp downshift,...

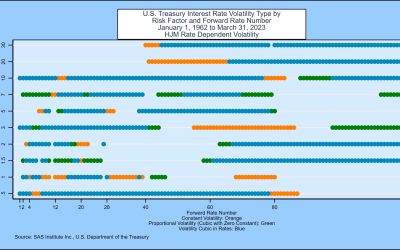

Daniel Dickler, Robert Jarrow, Stas Melnikov, Alexandre Telnov, Donald R. van Deventer and Xiaoming Wang[1] First Version: April...

Both implied forward Treasury 1-month bill rates and simulated 3-month bill rates show high volatility and a sharp downshift,...

If the Treasury 2-year/10-year spread continues to be negative for another month, this bout of negative spreads will become the...

We show below that the long-run peak in U.S. 1-month forward rates dropped this week from 4.85% to 4.74%. The probability that...

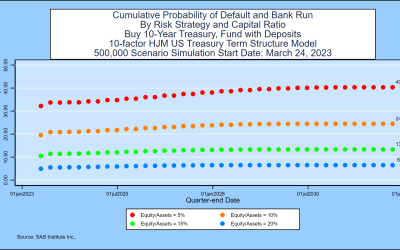

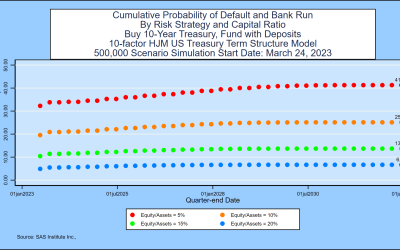

The weekly interest rate simulation now includes an assessment of the probability of default when a bank, institutional...

Today’s Treasury yield simulation reflects the continuing effects of the “flight to safety” in the wake of the collapse of...

Today’s Treasury yield simulation reflects the strong investor “flight to safety” in the wake of Friday’s collapse of Silicon...