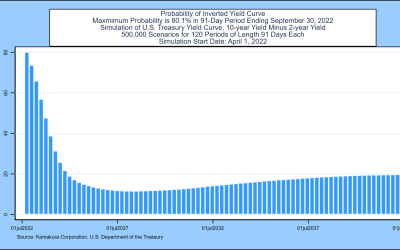

Kamakura Weekly Forecast, April 1, 2022: Inverted Yields, Negative Rates, and U.S. Treasury Probabilities 10 Years Forward Yield...

Kamakura Weekly Forecast, April 1, 2022: Inverted Yields, Negative Rates, and U.S. Treasury Probabilities 10 Years Forward Yield...

Inverted Yields, Negative Rates, and U.S. Treasury Probabilities 10 Years Forward In this week’s forecast, the focus is on three...

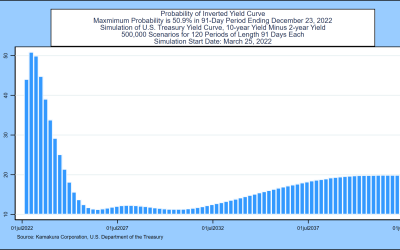

Kamakura Weekly Forecast, March 18, 2022: Inverted Yields, Negative Rates, and U.S. Treasury Probabilities 10 Years Forward In...

Donald R. van Deventer[1] First Version: March 8, 2022 This Version: March 8, 2022 ABSTRACT Please note: Kamakura Corporation...

In this week’s forecast, the focus is on three elements of interest rate behavior: the probability of the recession-predicting...

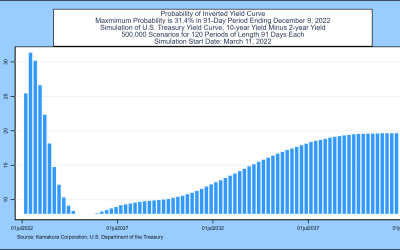

Donald R. van Deventer[1] First Version: March 8, 2022 This Version: March 8, 2022 ABSTRACT Please note: Kamakura Corporation...

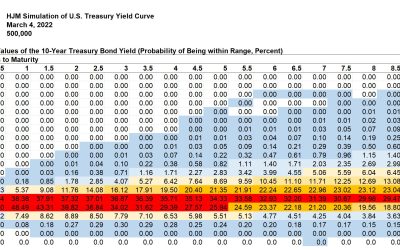

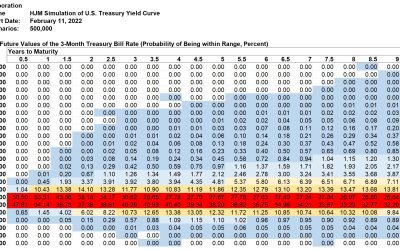

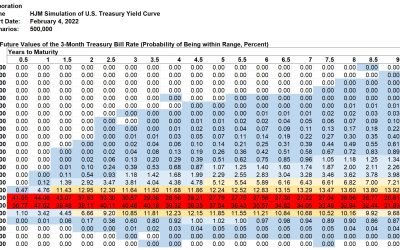

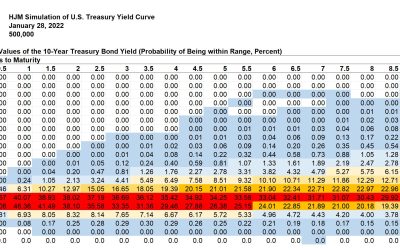

This week’s simulation shows that the most likely range for the 3-month U.S. Treasury bill yield in ten years is from 0% to 1%. ...

This week’s simulation shows that the most likely range for the 3-month U.S. Treasury bill yield in ten years is from 0% to 1%. ...

This week’s simulation shows that the most likely range for the 3-month U.S. Treasury bill yield in ten years is from 0% to 1%. ...

This week’s simulation shows that the most likely range for the 3-month U.S. Treasury bill yield in ten years is from 0% to 1%. ...

This week’s simulation shows that the most likely range for the 3-month U.S. Treasury bill yield in ten years is from 0% to 1%. ...

This week’s simulation shows that the most likely range for the 3-month U.S. Treasury bill yield in ten years is from 0% to 1%. ...