Daniel Dickler, Robert Jarrow, Stas Melnikov, Alexandre Telnov, Donald R. van Deventer and Xiaoming Wang[1] This Version:...

Daniel Dickler, Robert Jarrow, Stas Melnikov, Alexandre Telnov, Donald R. van Deventer and Xiaoming Wang[1] This Version:...

The 1-month forward U.S. Treasury yield now peaks at 5.00%, down 16 basis points from last week. As explained in Prof. Robert...

Daniel Dickler, Robert Jarrow, Stas Melnikov, Alexandre Telnov, Donald R. van Deventer and Xiaoming Wang[1] First Version:...

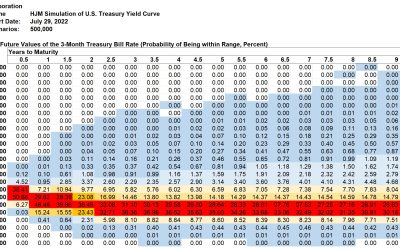

The Federal Reserve’s 75 basis point increase resulted in a yield curve twist, with shorter term Treasury yields shifting up and...

The forward 1-month U.S. Treasury yield now peaks at 4.98%, up 3 basis points from last week. As explained in Prof. Robert...

Treasury yields moved surprisingly little on the day of Chairman Powell’s Jackson Hole comments, but on reflection early last...

Reformed lawyer Jerome Powell argued in Jackson Hole that market participants are underestimating the Fed’s determination to...

Inverted Yields, Negative Rates, and U.S. Treasury Probabilities 10 Years Forward The negative 2-year/10-year Treasury spread...

Inverted Yields, Negative Rates, and U.S. Treasury Probabilities 10 Years Forward The market has now had a month to adjust to...

Inverted Yields, Negative Rates, and U.S. Treasury Probabilities 10 Years Forward The market has now had more than three weeks...

Inverted Yields, Negative Rates, and U.S. Treasury Probabilities 10 Years Forward The market has now had more than two weeks to...

Inverted Yields, Negative Rates, and U.S. Treasury Probabilities 10 Years Forward Friday was the eighth day of inverted Treasury...