Today’s analysis shows that the negative 2-year/10-year U.S. Treasury spread looks likely to persist well into fall, 2023 and...

Today’s analysis shows that the negative 2-year/10-year U.S. Treasury spread looks likely to persist well into fall, 2023 and...

Daniel Dickler, Robert Jarrow, Stas Melnikov, Alexandre Telnov, Donald R. van Deventer and Xiaoming Wang[1] This Version:...

Today’s simulation shows that the inverted 2-year/10-year spread is likely to persist through August. The analysis below show...

The most important statistic from this week’s simulation is the future probability of an inverted 2 year/10 year Treasury yield...

The 1-month forward U.S. Treasury yield curve currently shows a long-term peak down 0.10% this week. As explained in Prof....

Daniel Dickler, Robert A. Jarrow, Stas Melnikov, Alexandre Telnov, Donald R. van Deventer, and Xiaoming Wang[1] First Version:...

Daniel Dickler, Robert A. Jarrow, Stas Melnikov, Alexandre Telnov, Donald R. van Deventer, and Xiaoming Wang[1] First Version:...

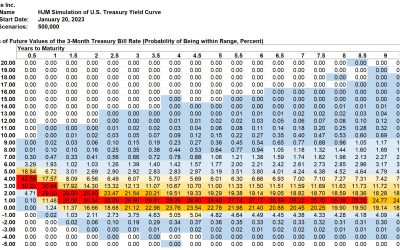

The 1-month forward U.S. Treasury yield currently show twin peaks at 5.04% in the short term and 4.77% over the longer term. As...

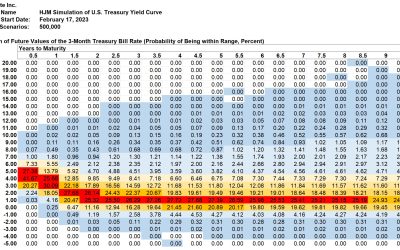

The 1-month forward U.S. Treasury yield curve currently shows twin peaks at 5.06% in the short term and 5.01% over the longer...

The long-term 1-month forward U.S. Treasury yield now peaks at 4.84%, up 20 basis points from last week. As explained in Prof....

Despite last week’s rate increase by the Federal Reserve, the long-term 1-month forward U.S. Treasury yield now peaks at 4.64%,...

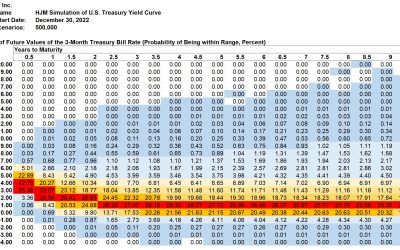

The long-term 1-month forward U.S. Treasury yield now peaks at 4.75%, down 25 basis points from last week. As explained in Prof....