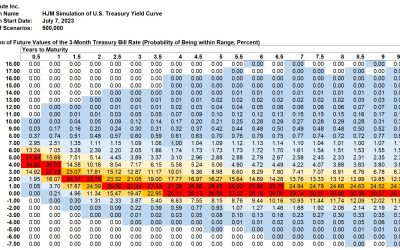

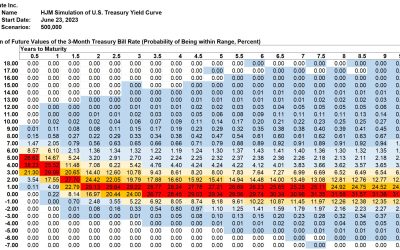

This week’s U.S. Treasury yield curve shifts reversed most of the increase from the prior week. The long-term peak in 1-month...

This week’s U.S. Treasury yield curve shifts reversed most of the increase from the prior week. The long-term peak in 1-month...

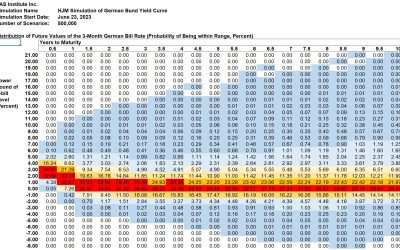

This week’s 2-year/10-year Bund yield spread is a negative 66.5 basis points, compared to a negative 86.2 basis points last...

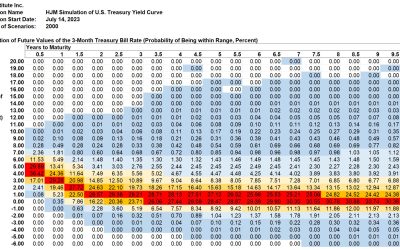

This week’s shift in the U.S. Treasury yield curve moved the long-term peak in 1-month Treasury forward rates up 0.19% to 5.10%....

This week’s simulation shows that the current negative 2-year/10-year Bund yield spread currently a negative 86.2 bsis points,...

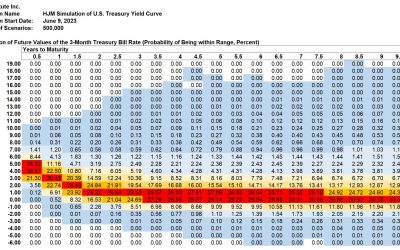

This week’s shift in the U.S. Treasury yield drove the negative 2-year/10-year Treasury spread to a negative 106 basis points....

This week’s simulation shows that the current negative 2-year/10-year Bund yield spread is very likely to persist at least...

This week’s simulation shows that the current negative 2-year/10-year Treasury yield spread is a near certainty to persist at...

Beginning with this forecast, we benchmark the U.S. Treasury simulation on a database with seven times more data than U.S....

The resolution of the Treasury debt cap crisis has resulted in a significant downward shift in the U.S. Treasury forward rate...

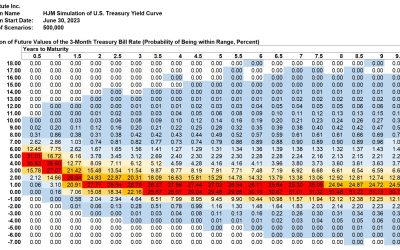

As of Friday, the current streak of trading days with a negative 2-year/10-year Treasury spread has reached 225 days, the third...

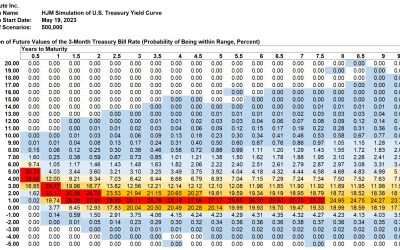

As of Friday, the current streak of trading days with a negative 2-year/10-year Treasury spread has reached 220 days, tied with...

Both implied forward Treasury 1-month bill rates and simulated 3-month bill rates show a sharp drop in the near term, especially...