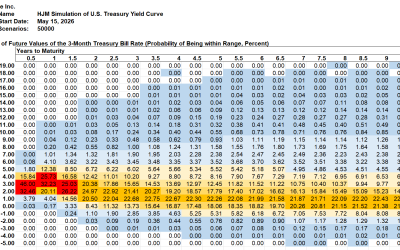

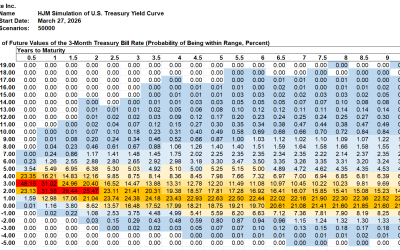

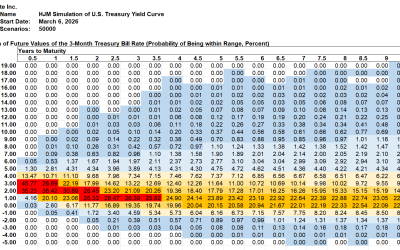

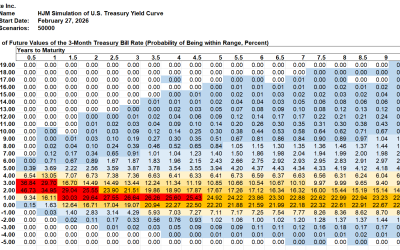

Summary After a short-term rise, the most likely range for 3-month bill yields in 10 years remained at the 1% to 2% range this...

Summary After a short-term rise, the most likely range for 3-month bill yields in 10 years remained at the 1% to 2% range this...

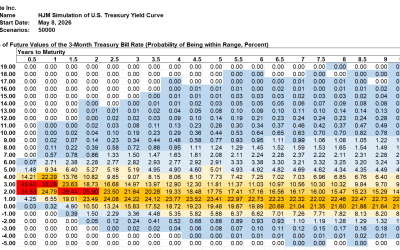

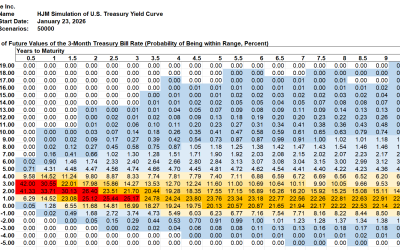

Summary The most likely range for 3-month bill yields in 10 years remained at the 1% to 2% range this week. The probability of...

Summary The most likely range for 3-month bill yields in 10 years remained at the 1% to 2% range this week. The probability of...

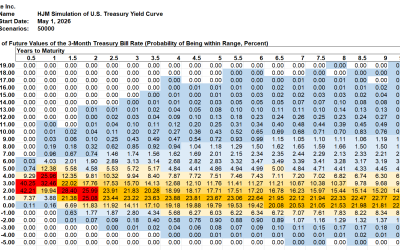

Summary The most likely range for 3-month bill yields in 10 years remained at the 1% to 2% range this week. The probability of...

Summary The most likely range for 3-month bill yields in 10 years remained at the 1% to 2% range this week. The probability of...

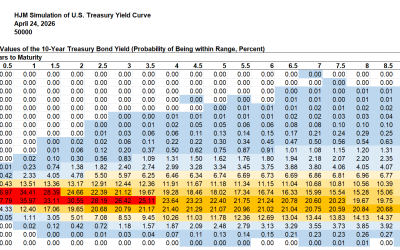

Summary The most likely range for 3-month bill yields in 10 years remained at the 1% to 2% range this week. The probability of...

Summary The most likely range for 3-month bill yields in 10 years remained at the 1% to 2% range this week. The probability of...

Summary The most likely range for 3-month bill yields in 10 years remained at the 1% to 2% range this week. The probability of...

Summary The most likely range for 3-month bill yields in 10 years remained at the 1% to 2% range this week. The probability of...

Summary The most likely range for 3-month bill yields in 10 years remained at the 1% to 2% range this week. The probability of...

Summary The most likely range for 3-month bill yields in 10 years remained at the 1% to 2% range this week. The probability of...

Summary The most likely range for 3-month bill yields in 10 years remained at the 1% to 2% range this week. The probability of...