Donald R. van Deventer July 8, 2025 Abstract The size of the term premium embedded in the current U.S. Treasury yield curve has...

Donald R. van Deventer July 8, 2025 Abstract The size of the term premium embedded in the current U.S. Treasury yield curve has...

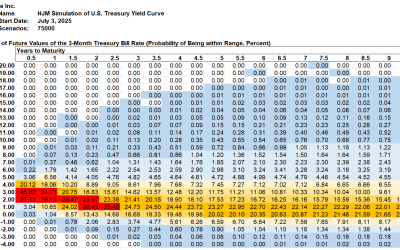

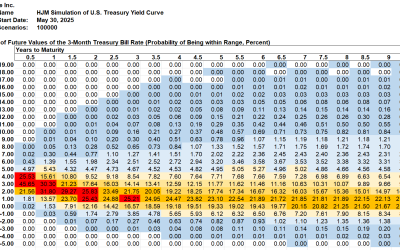

Summary The most likely range for 3-month bill yields is the 1% to 2% range, unchanged from last week. The probability of being...

Summary The most likely range for 3-month bill yields is the 1% to 2% range, up one percent from last week from last week. The...

Summary The most likely range for 3-month bill yields is the 0% to 1% range, unchanged from last week. Treasury 2-year yields...

Summary The most likely range for 3-month bill yields is the 0% to 1% range, down from the 1% to 2% range last week. Treasury...

Summary The most likely range for 3-month bill yields is again the 1% to 2% range, now 45 basis points more likely than the 0%...

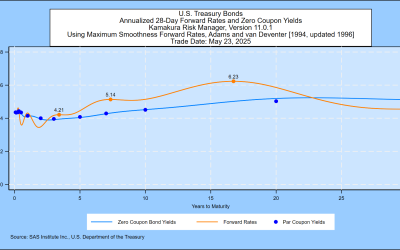

The Heath, Jarrow and Morton [1992] framework for simulation and valuation using risk-free interest rates has been called “the...

Summary The most likely range for 3-month bill yields is again the 1% to 2% range, just 22 basis points more likely than the 0%...

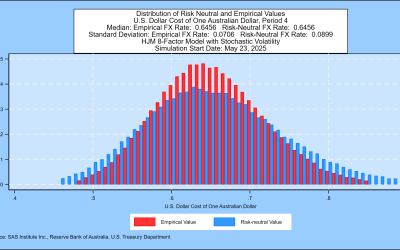

Summary The 2-year/10-year Bund spread closed the week at a positive 0.802%, a change from 0.7385% last week. As a result,...

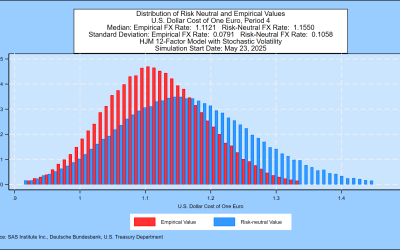

Summary The median level for the yen-U.S. dollar exchange rate is 148.09 one year from now, compared to 151.10 last week,...

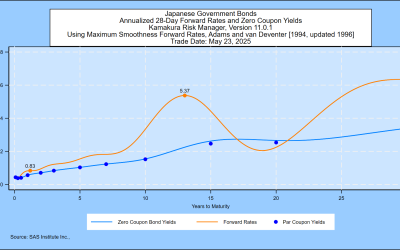

Summary One-month forward Australian Government Bond rates peaked at 5.40% this week, compared to 5.48% the previous week. The...

Summary The most likely range for 3-month bill yields is again the 1% to 2% range, just 20 basis points more likely than the 0%...