Research

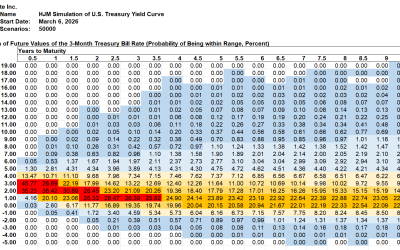

SAS Weekly Treasury Simulation, March 6, 2026: 3-Month Bill Mostly Likely Range Drops 200 bp in 30 Months

Summary The most likely range for 3-month bill yields in 10 years remained at the 1% to 2% range this week. The probability of...

The Credibility Risk in Credit

February saw a modest widening in public credit spreads: the ICE BofA U.S. Corporate (IG) OAS widened from 75 bps at January...

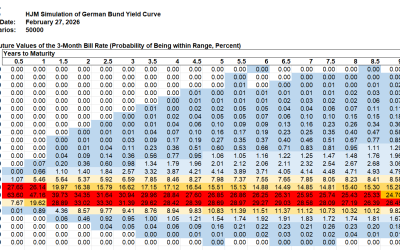

HJM++© Correlated Government Yield and Foreign Exchange Rate Simulations for Asia-Pacific, Europe and North America, February 27, 2026

The Heath, Jarrow and Morton [1992] framework for simulation and valuation using risk-free interest rates has been called “the...

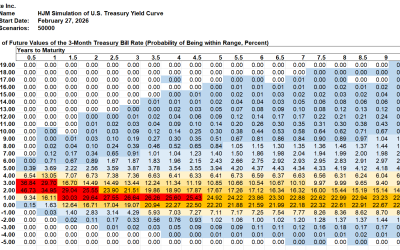

SAS Weekly Treasury Simulation, February 27, 2026: 3-Month Bill Decline Stays on Track to 1% to 2% in 30 Months

Summary The most likely range for 3-month bill yields in 10 years remained at the 1% to 2% range this week. The probability of...

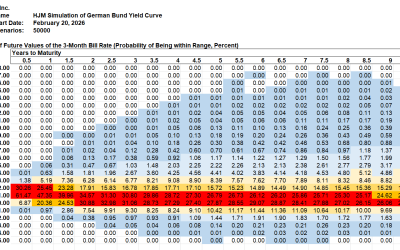

HJM++© Correlated Government Yield and Foreign Exchange Rate Simulations for Asia-Pacific, Europe and North America, February 20, 2026

The Heath, Jarrow and Morton [1992] framework for simulation and valuation using risk-free interest rates has been called “the...

SAS Weekly Treasury Simulation, February 20, 2026: Quantifying the Fall in Treasury Yields

Summary The most likely range for 3-month bill yields in 10 years remained at the 1% to 2% range this week. The probability of...

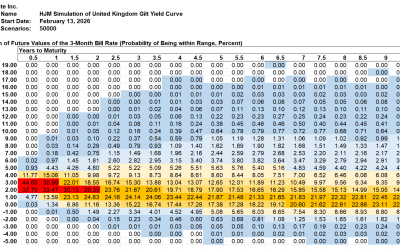

HJM++© Correlated Government Yield and Foreign Exchange Rate Simulations for Asia-Pacific, Europe and North America, February 13, 2026

The Heath, Jarrow and Morton [1992] framework for simulation and valuation using risk-free interest rates has been called “the...

SAS Weekly Treasury Simulation, February 13, 2026: 3-Month Bill 3.68% Today, 1%-2% Range in 30 Months

Summary The most likely range for 3-month bill yields in 10 years remained at the 1% to 2% range this week. The probability of...

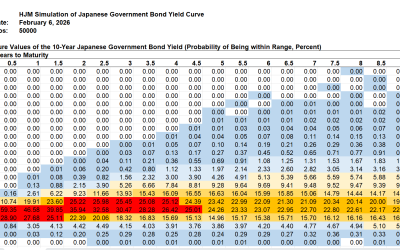

HJM++© Correlated Government Yield and Foreign Exchange Rate Simulations for Asia-Pacific, Europe and North America, February 6, 2026

The Heath, Jarrow and Morton [1992] framework for simulation and valuation using risk-free interest rates has been called “the...

SAS Weekly Treasury Simulation, February 6, 2026: 3-Month Bill Rate’s 30-Month Decline to 1%-2% Range

Summary The most likely range for 3-month bill yields in 10 years remained at the 1% to 2% range this week. The probability of...

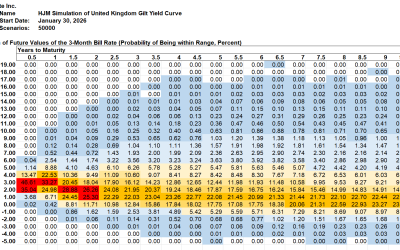

HJM++© Correlated Government Yield and Foreign Exchange Rate Simulations for Asia-Pacific, Europe and North America, January 30, 2026

The Heath, Jarrow and Morton [1992] framework for simulation and valuation using risk-free interest rates has been called “the...

Divergence in Credit Conditions: Index-Level Resilience vs Typical-Firm Strain

Markets opened 2026 with risk appetite intact, and early performance patterns suggested leadership may be broadening beyond the...