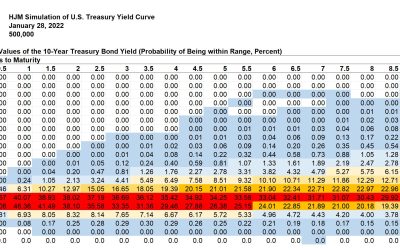

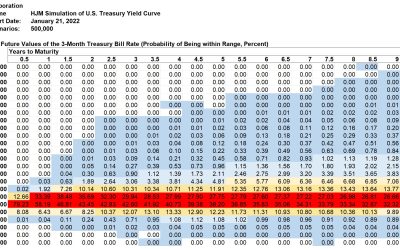

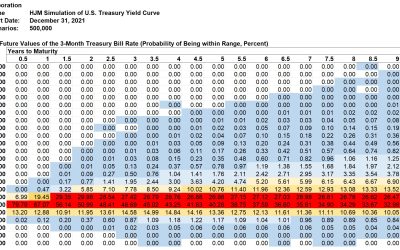

This week’s simulation shows that the most likely range for the 3-month U.S. Treasury bill yield in ten years is from 0% to 1%. ...

This week’s simulation shows that the most likely range for the 3-month U.S. Treasury bill yield in ten years is from 0% to 1%. ...

Donald R. van Deventer First Version: January 24, 2022 This Version: January 25, 2022 ABSTRACT Please note: Kamakura...

This week’s simulation shows that the most likely range for the 3-month U.S. Treasury bill yield in ten years is from 0% to 1%. ...

Donald R. van Deventer January 18, 2022 With inflation obviously on the rise, any rational investor should be asking “How well...

This week’s simulation shows that the most likely range for the 3-month U.S. Treasury bill yield in ten years is from 0% to 1%. ...

SINGAPORE, 11 January 2022: Kamakura Corporation has completed an upgrade project of its suite of solutions for Vietnam-based...

This week’s simulation shows that the most likely range for the 3-month U.S. Treasury bill yield in ten years is from 0% to 1%. ...

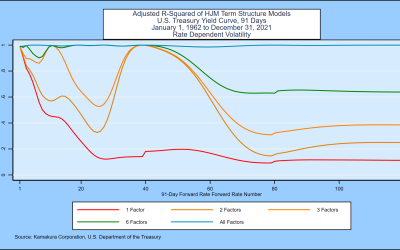

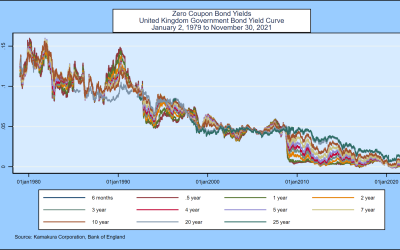

A 15-Factor Heath, Jarrow, and Morton Stochastic Volatility Model for the United Kingdom Government Bond Yield Curve, Using...

Jens Hilscher†, Robert A. Jarrow‡, and Donald R. van Deventer§ January 3, 2022 Abstract This paper shows that, for a sample of...

Kamakura Troubled Company Index Decreases by 0.90% to 4.40% Credit Quality Remains Strong and rises to the 99th Percentile NEW...

This week’s simulation shows that the most likely range for the 3-month U.S. Treasury bill yield in ten years is from 0% to 1%. ...