When Will Their Glory Fade?

Kamakura Troubled Company Index Increases by 2.76% to 17.64%

Credit Quality At the 29th Percentile

NEW YORK, March 1, 2021: I almost called this month’s review “The Bond Vigilante Revisited,” referencing the concept introduced by Edward Yardeni and made famous by James Carville. On second thought, I realized this slightly modified line from Alfred, Lord Tennyson’s “Charge of the Light Brigade” was more appropriate.

The Kamakura Troubled Company Index® indicated that credit quality declined at the end of February over the previous thirty days, with default probabilities rising from 2.76% to 17.64%. Volatility moderated slightly, ranging from 13.73% on February 5 to 18.01% on February 25 and ending the month at the 29th percentile. The index reflects the percentage of 40,500 public firms that have a default probability of over 1%. An increase in the index reflects declining credit quality, while a decrease reflects improving credit quality.

At the close of February, the percentage of companies with a default probability between 1% and 5% was 14.54%, an increase of 2.30% over the previous month. The percentage with a default probability between 5% and 10% was 2.01%, an increase of 0.24%. Those with a default probability between 10% and 20% amounted to 0.81% of the total, an increase of 0.13%; and those with a default probability of over 20% amounted to 0.28%, an increase of 0.09%.

Troubled Company Index – February 26, 2020

Among the 10 riskiest-rated firms listed in February, six were in the U.S., with one each in Australia, Greece, Japan and Norway. The riskiest-rated firm was GTT Communications Inc. (NYSE:GTT) a U.S. telecommunications firm whose one month KDP of 36.26% shot up by 21.71% from the prior month. The second riskiest-rated firm was the Washington Prime Group Inc. (NYSE:WPG). Both were subject of potential investor litigation and default rumors, but had experienced rising KDP’s for over a year.

Riskiest Rated Companies based on 1-month KDP

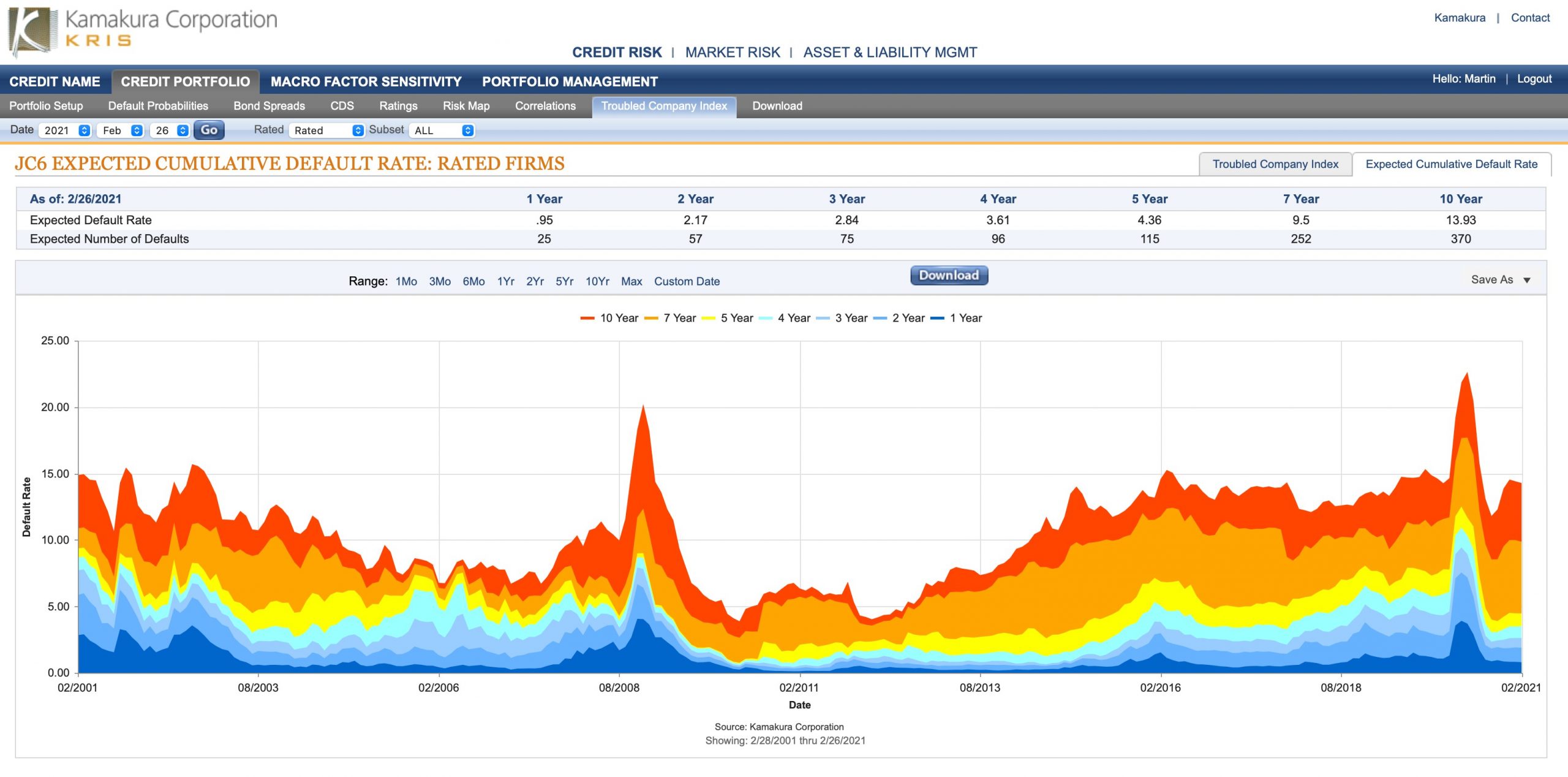

The Kamakura expected cumulative default curve for all rated companies worldwide narrowed with the one-year expected default rate increasing by 0.16% to 0.95%, while the 10-year rate decreased by 0.53% to 13.66%. Of particular interest the implied forward rate indicates that the expected default rate in 2022 will increase from 0.86% in 2021 to 1.22%, which makes intuitive sense when considering the low level of interest rates and aggressive fiscal policies.

Expected Cumulative Default Rate – February 26, 2021

Commentary

By Martin Zorn, President and Chief Operating Officer, Kamakura Corporation

I began this month’s review by referring to Edward Yardeni’s concept of “bond vigilantes”. Recently, Yardeni told the Financial Times, “We’re in a brave new world of excesses in fiscal and monetary policy, and that’s where bond vigilantes thrive. It’s their job to bring law and order back to the economy when the central banks and the fiscal authorities are lawless. And that’s arguably what we are seeing here.”

Yardeni was referring to the market reaction after President Biden said we have to ”Act big” and Federal Reserve Chair Powell pledged to remain accommodative. The result was a jump in the 10-year Treasury yield, which rose as high as 1.64%.

At the risk of disclosing my age, I will tell you that I started banking in 1980. So, I don’t know which surprises me more: the market reaction to the increased Treasury yield, or the fact that a 1.60% yield on the 10-year Treasury is considered alarmingly high.

The most important issue is to understand here is the unintended consequences of government actions.

To be sure, the pandemic has been catastrophic to the global economy, and strong actions by central banks and fiscal policies have provided many with a safety net, though others continue to suffer.

But it is also true that much of the economic pain has been self-inflicted by well-meaning but perhaps incorrect government reactions. With vaccines rolling out quickly and more coming into the pipeline, we can already see the light at the end of the tunnel, yet very broad stimulus measures are being introduced, with a little pork (maybe a lot of pork) piled on for good measure. What will the unintended consequences be? Where is the stress test – the one officials insist that banks regularly perform – on the federal balance sheet?

The current scenario raises a number of important questions for the future. What will happen to pensions, given low rates, rising volatility and a demographic surge of recipients ahead? What about defaults — can accommodative policy keep creating more and more debt, believing no one has to pay it off as long as it can be refinanced? How does this impact green policy? More broadly, if the government can print money to cushion the impact of government-mandated shutdowns, will it further slow the economy with socially activist policies and remain oblivious to the economic consequences?

I believe the bond market can provide a reality check, but it’s one that central banks and governments seem to be ignoring. For those brave traders trying to impose fiscal discipline – going against the actions of the Federal Reserve Bank, the ECB, and government policy makers — my thoughts turn to the “widow-maker trade” of years past, in which markets tried shorting Japanese government bonds.

I feel for those who are trying to fight both government policies and central bankers, and whose actions recall “The Charge of the Light Brigade”:

Cannon to right of them,

Cannon to left of them,

Cannon behind them

Volleyed and thundered;

Stormed at with shot and shell,

While horse and hero fell.

They that had fought so well

Came through the jaws of Death,

Back from the mouth of hell,

All that was left of them,

Left of six hundred.

When can their glory fade?

O the wild charge they made!

All the world wondered.

Honour the charge they made!

Honour the Light Brigade,

Noble six hundred!

About the Troubled Company Index

The Kamakura Troubled Company Index® measures the percentage of 40,500 public firms in 76 countries that have an annualized one- month default risk of over one percent. The average index value since January 1990 is 14.57%. Since November 2015, the Kamakura index has used the annualized one-month default probability produced by the KRIS version 6.0 Jarrow-Chava reduced form default probability model, a formula that bases default predictions on a sophisticated combination of financial ratios, stock price history, and macro-economic factors.

The KRIS version 6.0 models were developed using a data base of more than 2.2 million observations and more than 2,600 corporate failures. A complete technical guide, including full model test results and parameters, is provided to subscribers. The KRIS service also includes a wide array of other default probability models that can be seamlessly loaded into Kamakura’s state-of-the-art enterprise risk management software engine, the Kamakura Risk Manager. Available models include the non-public-firm default model, the commercial real estate model, the U.S. bank model, and the sovereign model. Related data includes credit default swap trading volume by reference name, market implied credit spreads, and prices on all traded corporate bonds traded in the U.S. market. Macro factor parameter subscriptions include Heath, Jarrow, and Morton term structure models for government securities in the U.S., Germany, the UK, Canada, Spain, Sweden, Australia, Japan, Thailand, and Singapore. All parameters are derived in a no-arbitrage manner consistent with seminal papers by Heath, Jarrow, and Morton, as well as Amin and Jarrow. A KRIS Macro Factor Scenario Service subscription includes both risk neutral and “real world” empirical scenarios for interest rates and macro factors.

The version 6.0 model was estimated over the period from 1990 to May 2014 and includes the insights of the entirety of the recent credit crisis. The 76 countries currently covered by the index are: Argentina, Australia, Austria, Bahrain, Bangladesh, Belgium, Belize, Botswana, Brazil, Bulgaria, Canada, Chile, China, Colombia, Croatia, Cyprus, Czech Republic, Denmark, Egypt, Estonia, Finland, France, Germany, Ghana, Greece, Hungary, Hong Kong, Iceland, India, Indonesia, Ireland, Israel, Italy, Japan, Jordan, Kenya, Kuwait, Luxembourg, Malaysia, Malta, Mauritius, Mexico, Nigeria, the Netherlands, New Zealand, Norway, Oman, Pakistan, Peru, the Philippines, Poland, Portugal, Qatar, Romania, Russia, Saudi Arabia, Serbia, Singapore, Slovakia, Slovenia, South Africa, South Korea, Spain, Sri Lanka, Sweden, Switzerland, Tanzania, Taiwan, Thailand, Turkey, the United Arab Emirates, Uganda, the UK, the U.S., Vietnam and Zimbabwe.

About Kamakura Corporation

Founded in 1990, Honolulu-based Kamakura Corporation is a leading provider of risk management information, processing, and software. Kamakura was recognized as a category leader in the Chartis Report, Technology Solutions for Credit Risk 2.0 2018. Kamakura was named to the World Finance 100 by the editor and readers of World Finance magazine in 2017, 2016 and 2012. In 2010, Kamakura was the only vendor to win two Credit Magazine innovation awards. Kamakura Risk Manager, first sold commercially in 1993 and now in version 10.1.1, is the first enterprise risk management system for users focused on credit risk, asset and liability management, market risk, stress testing, liquidity risk, counterparty credit risk, and capital allocation from a single software solution. The KRIS public firm default service was launched in 2002. The KRIS sovereign default service, the world’s first, was launched in 2008, and the KRIS non-public firm default service was offered beginning in 2011. Kamakura added its U.S. Bank default probability service in 2014.

Kamakura has served more than 330 clients with assets ranging in size from $1.5 billion to $3.0 trillion. Current clients have a combined “total assets” or “assets under management” in excess of $26 trillion. Its risk management products are currently used in 47 countries, including the United States, Canada, Germany, the Netherlands, France, Austria, Switzerland, the United Kingdom, Russia, Ukraine, South Africa, Australia, China, Hong Kong, India, Indonesia, Japan, Korea, Malaysia, Singapore, Sri Lanka, Taiwan, Thailand, Vietnam, and many other countries in Asia, Europe and the Middle East.

To follow risk commentary by Kamakura on a daily basis, please follow:

Kamakura CEO, Dr. Donald van Deventer (www.twitter.com/dvandeventer)

Kamakura President, Martin Zorn (www.twitter.com/riskmgrhi)

Kamakura’s official twitter account (www.twitter.com/KamakuraCo).

For more information, please contact:

Kamakura Corporation

2222 Kalakaua Avenue, Suite 1400, Honolulu, Hawaii 96815

Telephone: 1-808-791-9888

Facsimile: 1-808-791-9898

Information: info@kamakuraco.com

Web site: www.kamakuraco.com