Transitory Risk

Kamakura Troubled Company Index Decreases by 6.54% to 7.57%

Credit Quality Improves to the 87th Percentile

NEW YORK, May 14, 2021: While inflation rates may rise and fall, consumers know that higher prices tend not to come down. When lower inflation rates occur, it really only means future price increases may moderate. Consumers are right: From a risk management standpoint, transitory risk is still risk.

The Kamakura Troubled Company Index® indicated that credit quality improved in April with a decline in default probabilities of 6.54% to 7.57%. Volatility increased, with default probabilities ranging from 13.49% on April 1 to 7.57% on April 30. The index reflects the percentage of 40,500 public firms that have a default probability of over 1%. An increase in the index reflects declining credit quality, while a decrease reflects improving credit quality.

At the close of April, the percentage of companies with a default probability between 1% and 5% was 6.65%, a decrease of 5.13% over the previous month. The percentage with a default probability between 5% and 10% was 0.66%, a decrease of 0.86%. Those with a default probability between 10% and 20% amounted to 0.20% of the total, a decrease of 0.42%; and those with a default probability of over 20% amounted to 0.06%, a decrease of 0.13%.

Troubled Company Index – April 30, 2021

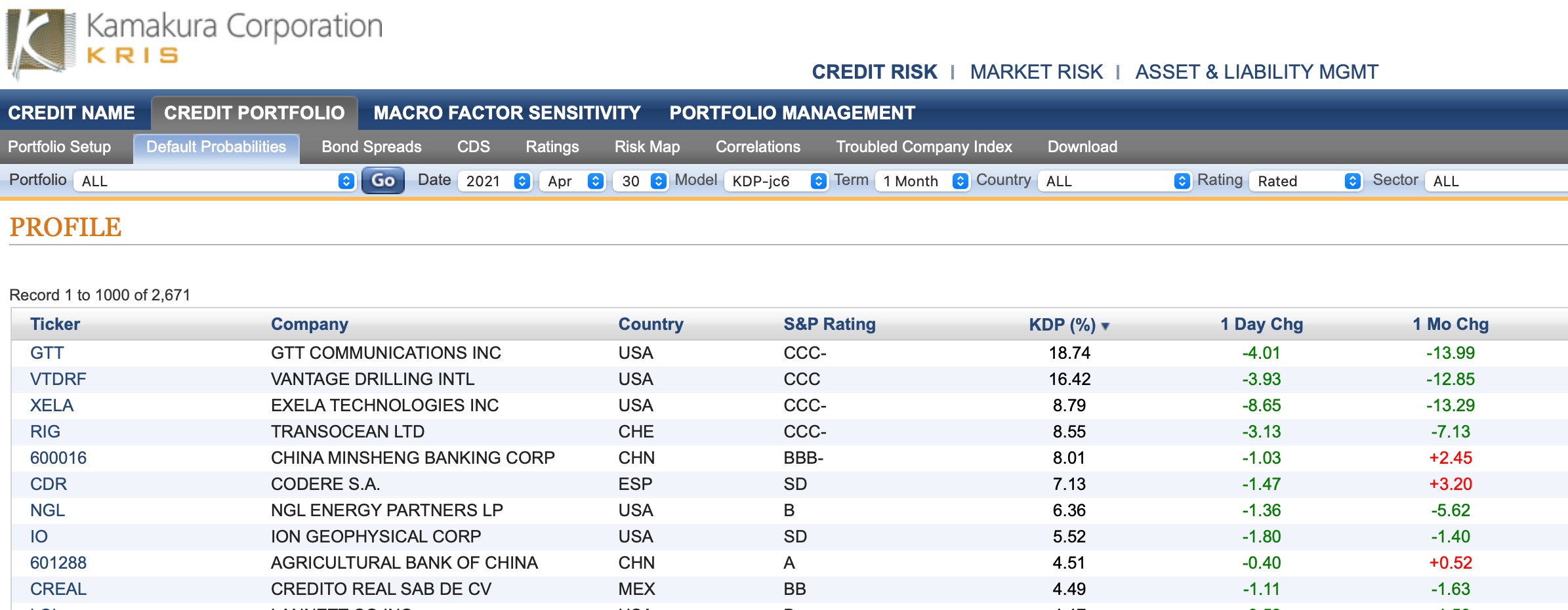

Among the 10 riskiest-rated firms listed in April, five were in the U.S., two in China and w one each in Mexico, Spain and Switzerland. The riskiest-rated firm remained GTT Communications Inc. (NYSE:GTT), a U.S. telecommunications firm whose one- month KDP was 18.74%.

Riskiest Rated Companies based on 1-month KDP

The Kamakura expected cumulative default curve for all rated companies worldwide narrowed, with the one-year expected default rate decreasing by 0.25% to 0.39%, while the 10-year rate decreased by 2.59% to 12.2%.

Expected Cumulative Default Rate – April 30, 2021

Commentary

By Martin Zorn, President and Chief Operating Officer, Kamakura Corporation

With Covid 19 cases worsening, especially in Brazil and India, and a weakening manufacturing sector in China, is it really time to worry about inflation?

It may be. U.S. equities rose for the month on strong earnings, one of several indicators reflecting a swiftly strengthening economic rebound in the world’s largest economy.

With recovery comes rising prices. The National Association of Home Builders reported that surging lumber prices have added $35,872 to the average price of a new home in the U.S. Land is getting more expensive, too – average lot prices for single-family homes are up 11%. The cost of gypsum drywall is up 7%, and copper has set a new record, up 27% year-to-date. Here at Kamakura, our commercial insurance rates rose by double digits, consistent with anecdotal reports from other companies. None of these expenses seem transitory.

I am not as sanguine as Federal Reserve Chairman Powell, who believes that “this time is different.” Neither is Dallas Federal Reserve President Robert Kaplan, who recently broke ranks with Powell, saying, “We’re now at a point where I’m observing excesses and imbalances in financial markets. I’m very attentive to that, and that’s why I do think at the earliest opportunity it will be appropriate for us to start talking about adjusting [asset] purchases.”

While Kaplan is not a member of the Open Market Committee his hawkish view merits serious consideration. History tells us that reflationary pressure can materialize very quickly. The combination of rising wholesale prices and a massive proposed fiscal stimulus – in an economy that is already rebounding strongly from the pandemic — calls for caution and robust stress testing against unintended consequences.

About the Troubled Company Index

The Kamakura Troubled Company Index® measures the percentage of 40,500 public firms in 76 countries that have an annualized one- month default risk of over one percent. The average index value since January 1990 is 14.55%. Since November 2015, the Kamakura index has used the annualized one-month default probability produced by the KRIS version 6.0 Jarrow-Chava reduced form default probability model, a formula that bases default predictions on a sophisticated combination of financial ratios, stock price history, and macro-economic factors.

The KRIS version 6.0 models were developed using a data base of more than 2.2 million observations and more than 2,600 corporate failures. A complete technical guide, including full model test results and parameters, is provided to subscribers. The KRIS service also includes a wide array of other default probability models that can be seamlessly loaded into Kamakura’s state-of-the-art enterprise risk management software engine, the Kamakura Risk Manager. Available models include the non-public-firm default model, the commercial real estate model, the U.S. bank model, and the sovereign model. Related data includes credit default swap trading volume by reference name, market implied credit spreads, and prices on all traded corporate bonds traded in the U.S. market. Macro factor parameter subscriptions include Heath, Jarrow, and Morton term structure models for government securities in the U.S., Germany, the UK, Canada, Spain, Sweden, Australia, Japan, Thailand, and Singapore. All parameters are derived in a no-arbitrage manner consistent with seminal papers by Heath, Jarrow, and Morton, as well as Amin and Jarrow. A KRIS Macro Factor Scenario Service subscription includes both risk neutral and “real world” empirical scenarios for interest rates and macro factors.

The version 6.0 model was estimated over the period from 1990 to May 2014 and includes the insights of the entirety of the recent credit crisis. The 76 countries currently covered by the index are: Argentina, Australia, Austria, Bahrain, Bangladesh, Belgium, Belize, Botswana, Brazil, Bulgaria, Canada, Chile, China, Colombia, Croatia, Cyprus, Czech Republic, Denmark, Egypt, Estonia, Finland, France, Germany, Ghana, Greece, Hungary, Hong Kong, Iceland, India, Indonesia, Ireland, Israel, Italy, Japan, Jordan, Kenya, Kuwait, Luxembourg, Malaysia, Malta, Mauritius, Mexico, Nigeria, the Netherlands, New Zealand, Norway, Oman, Pakistan, Peru, the Philippines, Poland, Portugal, Qatar, Romania, Russia, Saudi Arabia, Serbia, Singapore, Slovakia, Slovenia, South Africa, South Korea, Spain, Sri Lanka, Sweden, Switzerland, Tanzania, Taiwan, Thailand, Turkey, the United Arab Emirates, Uganda, the UK, the U.S., Vietnam and Zimbabwe.

About Kamakura Corporation

Founded in 1990, Honolulu-based Kamakura Corporation is a leading provider of risk management information, processing, and software. Kamakura was recognized as a category leader in the Chartis Report, Technology Solutions for Credit Risk 2.0 2018. Kamakura was named to the World Finance 100 by the editor and readers of World Finance magazine in 2017, 2016 and 2012. In 2010, Kamakura was the only vendor to win two Credit Magazine innovation awards., Kamakura Risk Manager, first sold commercially in 1993 and now in version 10.0.5, is the first enterprise risk management system for users focused on credit risk, asset and liability management, market risk, stress testing, liquidity risk, counterparty credit risk, and capital allocation from a single software solution. The KRIS public firm default service was launched in 2002. The KRIS sovereign default service, the world’s first, was launched in 2008, and the KRIS non-public firm default service was offered beginning in 2011. Kamakura added its U.S. Bank default probability service in 2014.

Kamakura has served more than 330 clients with assets ranging in size from $1.5 billion to $7.0 trillion. Current clients have a combined “total assets” or “assets under management” in excess of $28 trillion. Its risk management products are currently used in 47 countries, including the United States, Canada, Germany, the Netherlands, France, Austria, Switzerland, the United Kingdom, Russia, Ukraine, South Africa, Australia, China, Hong Kong, India, Indonesia, Japan, Korea, Malaysia, Singapore, Sri Lanka, Taiwan, Thailand, Vietnam, and many other countries in Asia, Europe and the Middle East.

To follow risk commentary by Kamakura on a daily basis, please follow:

Kamakura CEO, Dr. Donald van Deventer (www.twitter.com/dvandeventer)

Kamakura President, Martin Zorn (www.twitter.com/riskmgrhi)

Kamakura’s official twitter account (www.twitter.com/KamakuraCo).

For more information, please contact:

Kamakura Corporation

2222 Kalakaua Avenue, Suite 1400, Honolulu, Hawaii 96815

Telephone: 1-808-791-9888

Facsimile: 1-808-791-9898

Information: info@kamakuraco.com

Web site: www.kamakuraco.com