KRIS is the only default probability and fixed income system which provides daily cross-validation between default probabilities, bond price & spread. KRIS default probability background is given here:

https://www.kamakuraco.com/solutions/kamakura-risk-information-svcs/default-probability-models/

We use the reduced form bond pricing model of Hilscher, Jarrow and van Deventer to price the bonds of every issuer in the U.S. corporate bond market that has at least 2 senior non-call fixed rate bond issues that had trade volume of $1 million or more each:

https://www.kamakuraco.com/wp-content/uploads/2020/12/CouponBondValuation35b.pdf

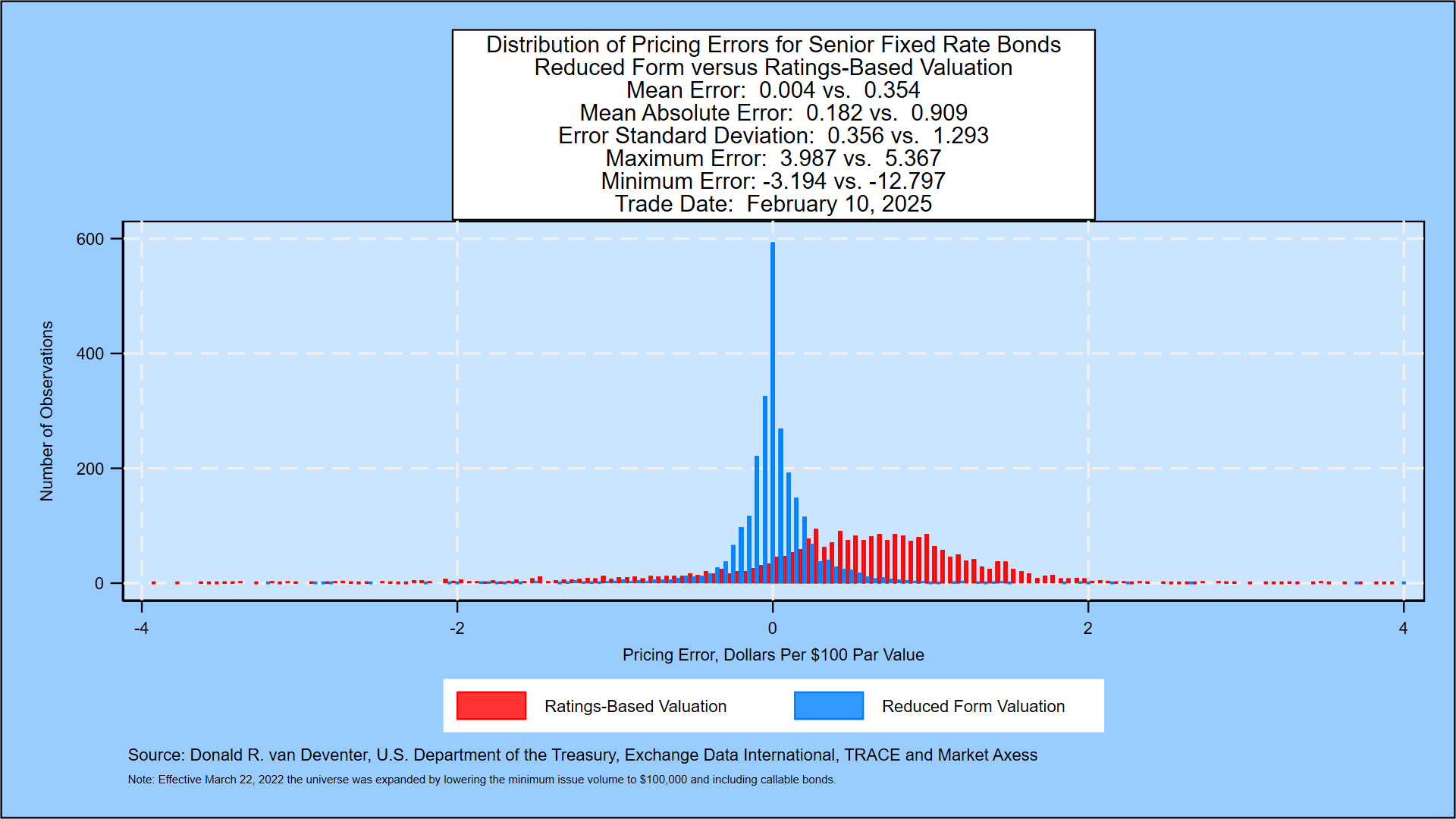

We compare KRIS bond pricing accuracy to a naïve model based on legacy credit ratings, using the best fitting credit spread levels for each rating grade. Today’s pricing accuracy comparison is shown below:

The trends in pricing error since September 1, 2017 are shown in this graph:

Finally, the day by day, bond by bond accuracy “win” percentage for KRIS versus ratings is presented here:

For more on the extensive model validation process followed in all aspects of SAS risk management products, please contact us at info@kamakuraco.com.