Credit Portfolio Analysis and Default Probabilities

Kamakura Default Probabilities

Kamakura provides default probability measures for public firms, non-public firms, U.S. banks, and sovereign counterparties which can be used to assess credit worthiness of an entire credit portfolio or on a single name basis. Inputs to the Kamakura models include company specific attributes, industry related measures and relevant macro-economic factors. Independent tests have confirmed that Kamakura default probabilities have the highest performing predictive power available in the market.

Kamakura Implied Spreads & Ratings

Kamakura’s Implied Spread model is an estimate of the credit spread of a company derived from company specific attributes, Kamakura default probabilities, industry classification and relevant macro-economic factors. The Implied Ratings model provides a most likely legacy rating agency rating for a public firm based on company specific attributes, Kamakura default probabilities, industry classification and relevant macro-economic factors along with the historical behavior of the legacy rating agencies.

Kamakura Default Correlations

Kamakura provides default correlations over its full universe of public firm counterparties for each of Kamakura’s default probability models. Different default modeling techniques and assumptions can produce varying results. The KRIS Web site includes coverage of over 35,000 companies in 67 countries. Kamakura provides correlations at 7 maturities for 35,000+ firms. The total number of pair wise default correlations available is more than 6.5 billion.

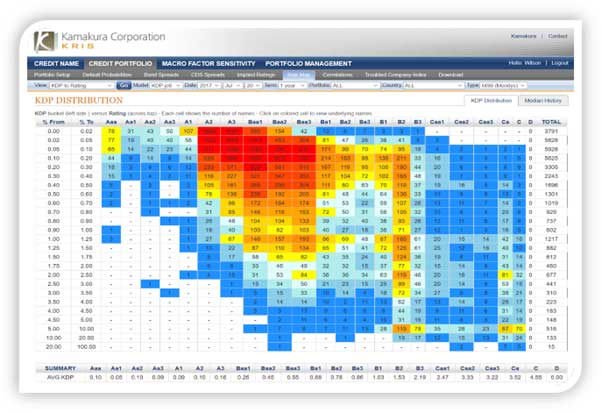

Credit Portfolio Analysis

KRIS credit portfolio analysis delivers objective credit quality measurement, modern default correlation technology, high performance default prediction and no conflict of interest. credit portfolio modeling analyses are available via online access. KRIS credit portfolio analysis features high ease of use due to its seamless integration with the Kamakura default probability service and access via browser or custom FTP file download. Use of multiple models, the hosted delivery model, and improved accuracy over agency ratings and agency-supplied default probabilities make the KRIS service unique among other similar analytical software offerings.

Kamakura’s Integrated Risk Solution

Kamakura Risk Manager (KRM) completely integrates credit portfolio management, market risk management, asset and liability management, Basel II and other capital allocation technologies, transfer pricing, and performance measurement. KRM uses a solid analytical foundation for valuation, pricing, and hedging of a wide range of equity securities, fixed income securities, foreign exchange contracts. KRM also delivers an unmatched list of derivatives and exotics.

In addition to the powerful KRM platform, Kamakura Risk Information Services (KRIS) provides extensive risk information on credit risk and interest rates. Credit risk information in KRIS includes default probabilities, default correlations, implied spreads and implied ratings for a wide range of counterparties. KRIS is seamlessly integrated into the KRM platform to fully incorporate the credit risk information into all KRM analyses.