Donald R. van Deventer

March 9, 2023

One of Warren Buffett’s most famous quotes goes like this: “Only when the tide goes out do you discover who’s been swimming naked.” That time is now for interest rate risk managers, who have been basking in the warm sea of declining interest rates for most of the last four decades. At high tide.

Thanks to the sharp spike in interest rates, the 2 basis point yield on 1-month Treasury bills of February 23, 2022 is just a rapidly fading memory. There are no talking points and no amount of PowerPoint presentations that can paper over serious mistakes in interest rate risk management. This is an era of serious job insecurity for interest rate risk managers, most of whom don’t know much about 1982, Paul Volcker, the savings and loan crisis, and the hundreds of savings and loans and banks that failed over the course of the 1980s and 1990s.

In my recent conversations with interest rate risk managers at large banks around the world, the danger signals are everywhere. The “tide table” for interest rate risk managers has these flashing red warning signs:

“We use interest rate futures to hedge generally accepted accounting principles net interest income 12 months forward.”

“We’ve been using the same interest rate risk vendor for 20 years.”

“We use a 1-factor yield curve model. The vendor tells us that’s all we need to manage risk well.”

“We don’t use default probabilities in our interest rate risk analysis. That’s done by the credit group.”

“We do interest rate risk once a month without fail.”

“We get our forecast for non-maturity deposits from the retail banking team.”

“Our analysis shows that the ‘surge deposits’ from the pandemic are here to stay.”

“Our bank benefits when there’s a banking crisis. The depositors of the bad banks come to us, and that experience is built into our risk analysis.”

These quotes are all real, and they terrify me. It seems like 1982 all over again. A lot of the most analytical people in the interest rate risk arena have moved to other disciplines in banking or left for unregulated financial services firms. The author got his first banking job in risk management at Security Pacific Bank when the interest rate risk tide went out on my predecessors in that function. They just disappeared suddenly, and no one ever told me what their names were. By 1982, after the interest rate function had been rebuilt, the asset and liability management committee at Security Pacific Corporation included four people who would ultimately serve as bank CEOs and four Ph.D. holders in a group of 12. By contrast, the 30-member interest rate risk group that I attend regularly currently has no members with a Ph.D. degree. I suspect that will change soon.

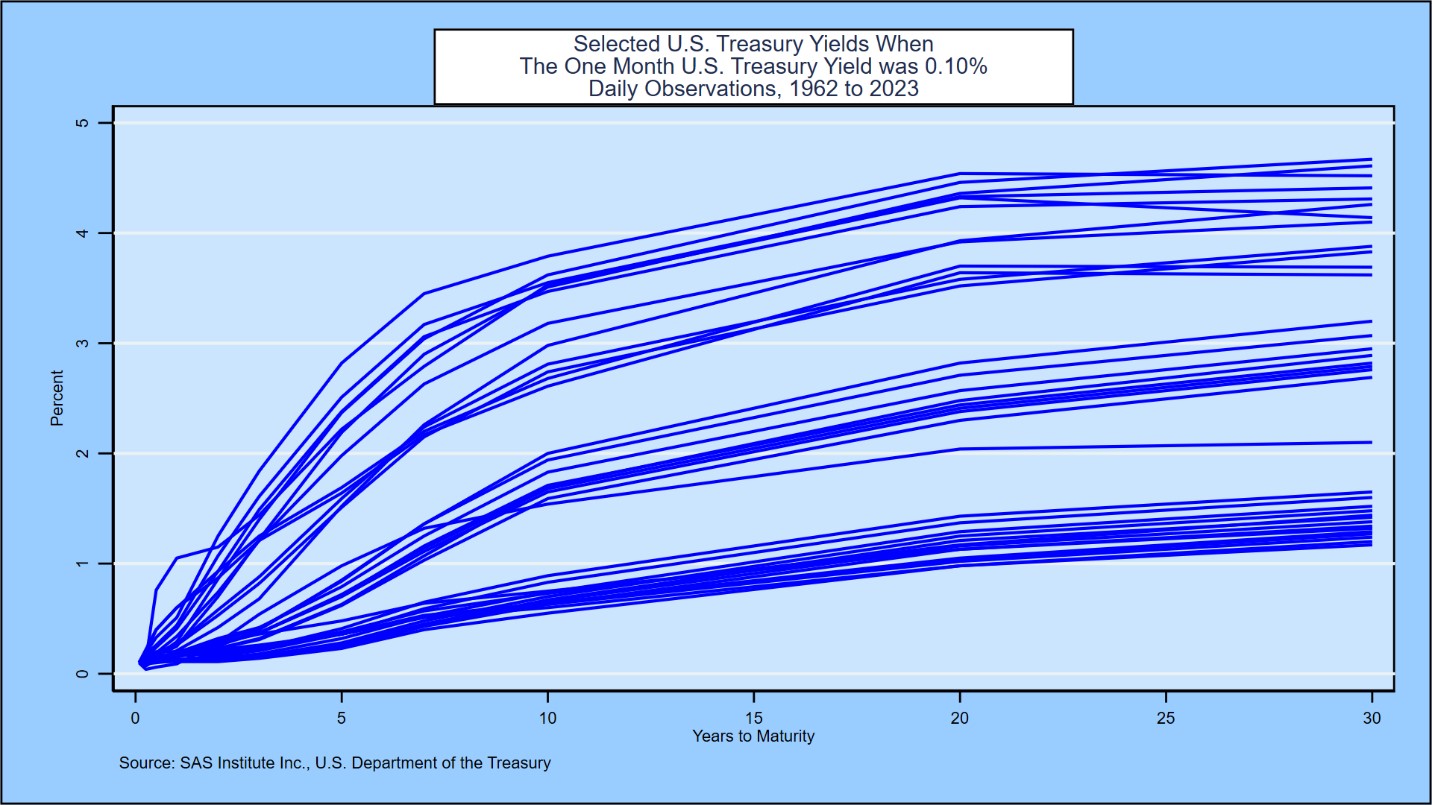

Of the comments above, the one that scares me the most is the quote about a one-factor interest rate risk framework. There’s a simple experiment one can conduct to assess the risk of a one-factor model. Take the history of the 1-month Treasury bill, the shortest maturity Treasury yield currently reported. Tabulate the rate levels to see what short rate levels have been experienced most often. The 1-month T-bill has been 2 basis points on 306 trading days. It’s been 10 basis points on 79 trading days. At a 5.18% level, there are 56 observations. The most famous 1-factor term structure model was published by my friend Oldrich Vasicek in 1977, when he was working at Wells Fargo Bank. Given the short rate of interest and two parameters, Oldrich was able to derive the entire yield curve (assuming the model is correct). Here’s a graph of most of the U.S. Treasury yield curves that prevailed when the 1-month Treasury bill rate was 10 basis points:

Here’s a similar picture of most of the Treasury yield curves that prevailed when the 1-month Treasury bill was 5.18%:

What these graphs show, in a way any bank chief executive officer can understand, is that bankers relying on 1-factor interest rate models are seriously at risk in the current environment. Valuations are wrong, capital adequacy calculations are wrong, hedges are wrong, and the correlation of rates, oil prices, and commercial real estate is completely ignored. It is the latter correlation that has devastated the banking and savings and loan industries twice in the past, with a $1 trillion cost to U.S. tax payers each time.

The joint capabilities of SAS and Kamakura, that combine the proven history of analytical excellence and innovative interest rate risk modeling, can be a great asset in navigating current challenging market envionment. For more information, please visit www.sas.com/alm.