Credit Conditions – Chapter One

Kamakura Troubled Company Index Increases by 8.17% to 31.96%

Credit Quality Drops to 4th Percentile

NEW YORK, April 1, 2020: Today’s release is the first monthly credit conditions report in the new world that the Covid-19 environment has ushered in. With the end of the quarter at hand, CFOs will need to provide information on the fair market value of their assets. The next few weeks will introduce the second chapter: The attack of the accounting monsters.

On March 27, IFRS released guidance on the application of the calculating expected loss https://cdn.ifrs.org/-/media/feature/supporting-implementation/ifrs-9/ifrs-9-ecl-and-coronavirus.pdf?la=en. A key comment from the release: “Entities are required to develop estimates based on the best available information about past events, current conditions and forecasts of economic conditions. In assessing forecast conditions, consideration should be given both to the effects of covid-19 and the significant government support measures being undertaken.”

In this release, we will look forward as much as we look back.

The Kamakura Troubled Company Index® continued to show increases in default risk for the third consecutive month, with an 8.17% rise to 31.96%, resulting in a drop in credit quality from the 14th percentile to the 4th percentile. The index also displayed a large jump in volatility, ranging during the month from 23.54% to 35.3%. The index reflects the percentage of 40,500 public firms that have a default probability of over 1%. An increase in the index reflects declining credit quality, while a decrease reflects improving credit quality.

At the close of March, the percentage of companies with a default probability between 1% and 5% was 22.6%, an increase of 5.16% over the month. The percentage with a default probability between 5% and 10% was 5.15%, an increase of 1.53%. Those with a default probability between 10% and 20% amounted to 2.8% of the total, an increase of 0.91%; and those with a default probability of over 20% amounted to 1.41%, an increase of 0.57% from the prior month. While default probabilities increased across the spectrum, the largest jump was for those in the 1%-to-5% category, indicating an increase in firms showing early signs of stress.

At 31.96%, the Troubled Company Index fell to the 4th percentile of historical credit quality as measured since 1990.

Among the 10 riskiest-rated firms listed in March, eight are in the U.S, and one each in Great Britain and Luxembourg. The riskiest rated company in our coverage universe was Laredo Petroleum, Inc, (NYSE:LPI) with a one-year KDP of 62.32%, up 31.67% over the past month. Seven of the 10 riskiest were in the energy sector. We had seven defaults in our coverage universe, with four in the U.S. and one each in Germany, India and the UK.

Ten Riskiest Rated Firms – 1-Year KDP

In the current environment, it is instructive to examine the relative risk by sector. The two tables below sort sectors by risk, going from riskiest to safest. Table 1 examines the median 1-month KDP and shows that banks are among the riskiest sectors in the current environment–although at 1.6%, the risk factor is relatively muted compared to the analysis of the 90th percentile. Table 2 shows the 90th percentile and reveals the riskiest 10% of each sector. Here, the media and energy sectors present clear red flags for risk in a portfolio.

The Kamakura expected cumulative default curve for all rated companies worldwide widened substantially, with the one-year expected default rate increasing by 1.89% to 4.09% while the 10-year rate increased by 7.33% to 22.15%.

Commentary

By Martin Zorn, President and Chief Operating Officer, Kamakura Corporation

After a long period of complacency, a single event often triggers a major market shift, and that is what is happening today. It is usually very difficult to identify the trigger event in advance, though many experts take credit for seeing them after the fact.

We certainly didn’t foresee the covid-19 trigger, but we did sense that something was seriously amiss. Over the past several years, we have used the expected cumulative default curve as a tool, and it has been waving a red flag about the future. We have been concerned for some time about refinancing risk, leveraged lending, loosening lending standards, and underfunded pension funds. We have also worried about the unanticipated consequences of negative rates, questioning whether central banks still had adequate tools to fight the next recession and whether fiscal policy could supplement monetary policy in a downturn.

We now get to test these potential risks all at once. The world is very different today than it was two months ago, last month, or even last week. The questions we have been posing are no longer hypothetical, but real, and we are learning the answers on a daily basis. This is a new quarter, and the world has intentionally shut down the global economy to fight the covid-19 pandemic. No one knows how long it will last or how quickly countries and sectors will bounce back.

None of this is good news if you are a CFO charged by your auditors to mark your portfolio to market. In the short run, companies will have to report their financial results using the best tools and information available.

In risk management, there are “known risks” that should be incorporated into your mark-to-market reporting. There are also “unknown risks.” We hope you have employed the appropriate quantitative tools to assess these “unknown” risks and ensure that you have adequate capital to weather the storm. In the coming months, we will know who employed tools robust enough to help them withstand today’s turbulent markets and who did not.

The government has taken extraordinary actions to put money into the hands of families who are suddenly unemployed and to help small businesses that yesterday couldn’t find enough employees, but today, find themselves closed. Even with government aid, many families and businesses will be unable to make their next mortgage or rent payment.

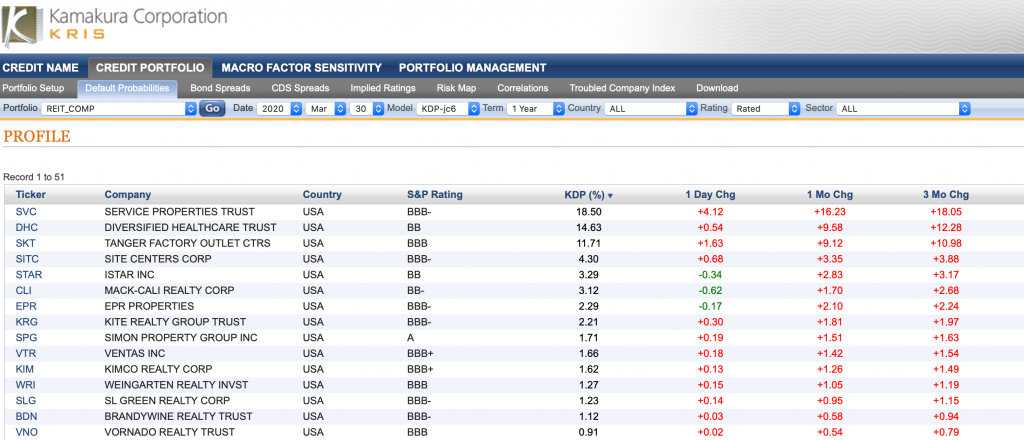

The next sector likely to experience the contagion of elevated risk is real estate. Table 3 below looks at the huge jump in default probabilities in the REIT composite, a proxy for the residential and commercial real estate sectors. Together, they may produce the next wave of the covid-19 financial tsunami.

Table 3: Default Probabilities for REITs

We do not know what fiscal or monetary steps governments will take next, but we do know there will be a great deal of financial contagion and fallout. All we can do is obtain the best models and data to guide us through these uncharted waters and work together using our sharpest tools to try to defeat the enemy at our doors.

About the Troubled Company Index

The Kamakura Troubled Company Index® measures the percentage of 40,575 public firms in 76 countries that have an annualized one- month default risk of over one percent. The average index value since January 1990 is 14.41%. Since November 2015, the Kamakura index has used the annualized one-month default probability produced by the KRIS version 6.0 Jarrow-Chava reduced form default probability model, a formula that bases default predictions on a sophisticated combination of financial ratios, stock price history, and macro-economic factors.

The KRIS version 6.0 models were developed using a data base of more than 2.2 million observations and more than 2,600 corporate failures. A complete technical guide, including full model test results and parameters, is provided to subscribers. The KRIS service also includes a wide array of other default probability models that can be seamlessly loaded into Kamakura’s state-of-the-art enterprise risk management software engine, the Kamakura Risk Manager. Available models include the non-public-firm default model, the commercial real estate model, the U.S. bank model, and the sovereign model. Related data includes credit default swap trading volume by reference name, market implied credit spreads, and prices on all traded corporate bonds traded in the U.S. market. Macro factor parameter subscriptions include Heath, Jarrow, and Morton term structure models for government securities in the U.S., Germany, the UK, Canada, Spain, Sweden, Australia, Japan, Thailand, and Singapore. All parameters are derived in a no-arbitrage manner consistent with seminal papers by Heath, Jarrow, and Morton, as well as Amin and Jarrow. A KRIS Macro Factor Scenario Service subscription includes both riskneutral and “real world” empirical scenarios for interest rates and macro factors.

The version 6.0 model was estimated over the period from 1990 to May 2014 and includes the insights of the entirety of the recent credit crisis. The 76 countries currently covered by the index are: Argentina, Australia, Austria, Bahrain, Bangladesh, Belgium, Belize, Botswana, Brazil, Bulgaria, Canada, Chile, China, Colombia, Croatia, Cyprus, Czech Republic, Denmark, Egypt, Estonia, Finland, France, Germany, Ghana, Greece, Hungary, Hong Kong, Iceland, India, Indonesia, Ireland, Israel, Italy, Japan, Jordan, Kenya, Kuwait, Luxembourg, Malaysia, Malta, Mauritius, Mexico, Nigeria, the Netherlands, New Zealand, Norway, Oman, Pakistan, Peru, the Philippines, Poland, Portugal, Qatar, Romania, Russia, Saudi Arabia, Serbia, Singapore, Slovakia, Slovenia, South Africa, South Korea, Spain, Sri Lanka, Sweden, Switzerland, Tanzania, Taiwan, Thailand, Turkey, the United Arab Emirates, Uganda, the UK, the U.S., Vietnam and Zimbabwe.

To follow the troubled company index and other risk commentary by Kamakura on a daily basis, please follow:

Kamakura CEO Dr. Donald van Deventer (www.twitter.com/dvandeventer) Kamakura President Martin Zorn (www.twitter.com/riskmgrhi) Kamakura’s official twitter account (www.twitter.com/KamakuraCo).

About Kamakura Corporation

Founded in 1990, Honolulu-based Kamakura Corporation is a leading provider of risk management information, processing, and software. Kamakura was recognized as a category leader in the Chartis Report, Technology Solutions for Credit Risk 2.0 2018. Kamakura was named to the World Finance 100 by the editor and readers of World Finance magazine in 2017, 2016 and 2012. In 2010, Kamakura was the only vendor to win two Credit Magazine innovation awards. Kamakura Risk Manager, first sold commercially in 1993 and now in version 10.0.5, is the first enterprise risk management system for users focused on credit risk, asset and liability management, market risk, stress testing, liquidity risk, counterparty credit risk, and capital allocation from a single software solution. The KRIS public firm default service was launched in 2002. The KRIS sovereign default service, the world’s first, was launched in 2008, and the KRIS nonpublic firm default service was offered beginning in 2011. Kamakura added its U.S. Bank default probability service in 2014.

Kamakura has served more than 330 clients with assets ranging in size from $1.5 billion to $3.0 trillion and fund managers with Assets Under Management in excess of $26 trillion. Its risk management products are currently used in 47 countries, including the United States, Canada, Germany, the Netherlands, France, Austria, Switzerland, the United Kingdom, Russia, Ukraine, South Africa, Australia, China, Hong Kong, India, Indonesia, Japan, Korea, Malaysia, Singapore, Sri Lanka, Taiwan, Thailand, Vietnam, and many other countries in Asia, Europe and the Middle East.

To follow risk commentary by Kamakura on a daily basis, please follow:

Kamakura CEO Dr. Donald van Deventer (www.twitter.com/dvandeventer)

Kamakura President Martin Zorn (www.twitter.com/riskmgrhi)

Kamakura’s official twitter account (www.twitter.com/KamakuraCo).

For more information, please contact:

Kamakura Corporation

2222 Kalakaua Avenue, Suite 1400, Honolulu, Hawaii 96815

Telephone: 1-808-791-9888

Facsimile: 1-808-791-9898

Information: info@kamakuraco.com

Web site: www.kamakuraco.com