Donald R. van Deventer[1]

First Version: April 15, 2022

This Version: May 2, 2022

ABSTRACT

Please note: Kamakura Corporation term structure models are updated monthly. For the most recent set of coefficients, contact info@kamakuraco.com

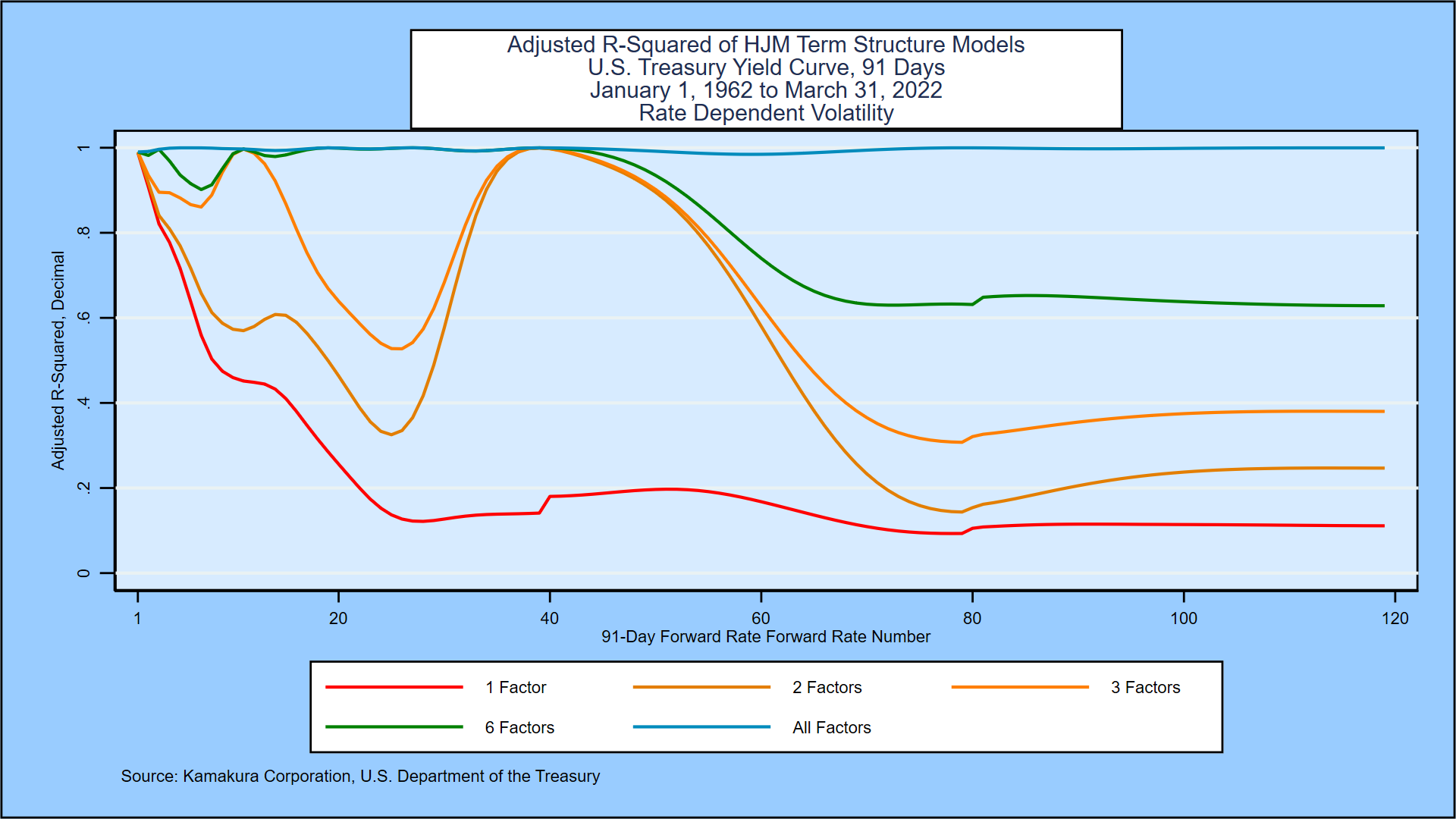

This paper analyzes the number and the nature of factors driving the movements in the U.S. Treasury yield curve from January 2, 1962 through March 31, 2022, updating prior documentation through December 31, 2021. The process of model implementation confirms a number of important insights for interest rate modeling generally. First, model validation of historical yields is important because those yields are the product of a third-party curve fitting process that may produce spurious indications of interest rate volatility. Second, quantitative measures of smoothness and international comparisons of smoothness provide a basis for measuring the quality of simulated yield curves. Third, we outline a process for incorporating insights from the Japanese and European experience with negative interest rates into term structure models with stochastic volatility in the United States and other countries. Finally, we illustrate the process for comparing stochastic volatility and affine models of the term structure. We conclude that stochastic volatility models have a superior fit, when out-of-sample simulation is the objective, to the history of yield movements in the U.S. Treasury market.

Full text:

Kamakura-AnUpdatedHJMModelforUSTreasuriesv2-20220331Footnotes

[1] Kamakura Corporation, 2222 Kalakaua Avenue, Suite 1400, Honolulu, Hawaii, USA, 96815. E-Mail dvandeventer@kamakuraco.com. The author wishes to thank Prof. Robert A. Jarrow for 27 years of conversations on this topic. Daniel Dickler, Theodore Spradlin, and Dr. Xiaoming Wang provided invaluable data services and smoothing analysis using Kamakura Risk Manager. The author also wishes to thank the participants at seminars organized by the Bank of Japan and the Federal Reserve Bank of San Francisco at which papers addressing similar issues were presented.